The Regulatory Crackdown: Understanding the CDL Mill Problem

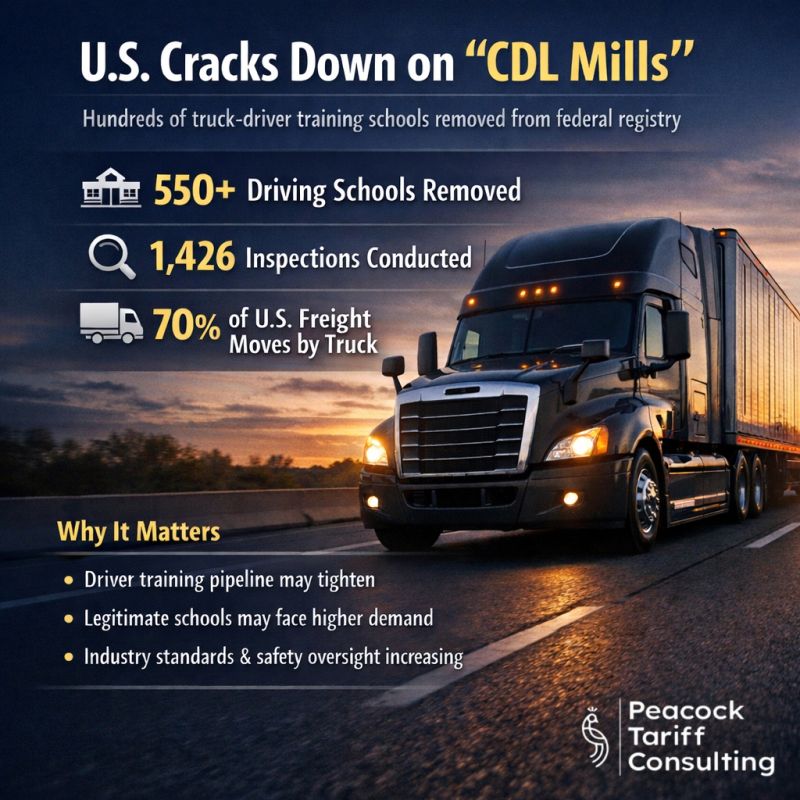

The U.S. government has taken decisive action against a pervasive problem in the transportation industry. Federal regulators recently removed over 550 truck-driving schools from the federal training registry following comprehensive investigations that revealed systemic safety and training failures. These institutions, commonly referred to as CDL mills, represent a troubling pattern of expedited licensing without adequate preparation or safety standards.

The scope of the federal inspection initiative was substantial. Over 1,400 inspections were conducted across schools identified as problematic. Inspectors documented recurring violations including unqualified instructors teaching critical safety procedures, inadequate hands-on training in vehicle operation and hazard recognition, and graduates entering the commercial driving market without foundational competencies. These findings were not isolated incidents but rather symptoms of widespread regulatory failure in a critical training pipeline.

From a regulatory perspective, the decision to delist these schools represents the government’s commitment to maintaining standards in an industry that directly impacts public safety. However, the implications extend far beyond safety metrics. This regulatory action carries significant consequences for freight markets, supply chains, and the logistics infrastructure that underpins American commerce.

The Logistics Foundation: Why Truck Drivers Are Critical Infrastructure

Understanding the importance of truck drivers requires recognizing their central role in the American economy. Trucks transport approximately 70 percent of all freight in the United States by weight. This statistic encompasses everything from perishable goods that demand time-sensitive delivery, to construction materials, consumer products, and industrial equipment. The trucking industry does not simply participate in supply chains; it is the backbone upon which modern logistics depend.

The supply of qualified truck drivers directly determines the capacity and efficiency of freight movement. When driver availability tightens, freight rates increase, delivery times lengthen, and supply chains experience stress. Conversely, when the driver workforce is abundant and well-trained, goods flow efficiently and cost-effectively. The training pipeline that produces new drivers therefore represents critical infrastructure investment.

For companies that depend on transportation services, understanding the dynamics of driver supply and quality is essential for supply chain planning. A shortage of qualified drivers translates directly into operational challenges, increased costs, and potential delays. The CDL mill closures must be understood within this context: the government is prioritizing quality and safety, but doing so creates short-term supply constraints that ripple through the logistics ecosystem.

Short-Term Market Impacts: The Transition Period

The immediate aftermath of removing 550 training providers from the registry will likely manifest in several observable ways across freight markets. First, the number of newly licensed commercial drivers entering the market will decline as schools previously supplying large cohorts of graduates exit the system. This represents a direct reduction in driver supply during a critical transition period.

Established and legitimate driver training schools that maintained high standards are likely to experience increased demand as alternative options disappear. However, these institutions typically operate at or near capacity already. The surge in demand may create bottlenecks where applicants face waiting lists and extended timelines to complete training programs. This creates a temporary supply constraint even as legitimate education providers work to expand capacity.

Regional variations in driver availability will become more pronounced. Some areas have robust training infrastructure with multiple reputable institutions, while others may have depended on now-delisted schools. Regions with limited legitimate training options may face acute driver shortages, potentially leading to geographic imbalances in trucking capacity. Shippers in affected regions may encounter higher rates, longer scheduling windows, and less service flexibility from carriers.

- Reduced flow of newly licensed drivers from legitimate schools

- Increased demand outpacing capacity at reputable training institutions

- Geographic availability gaps in driver supply

- Upward pressure on freight rates in affected regions

Long-Term Industry Transformation and Standards Elevation

Beyond the immediate transition challenges, the regulatory action establishes a new baseline for the trucking industry. The clear message from federal regulators is that driver training standards will be maintained at legitimate levels, and institutions that cut corners will be removed from the system. This creates incentives for training providers to maintain rigorous curricula, invest in qualified instructors, and provide comprehensive safety training.

Companies that operate training facilities or contract with training providers should view this regulatory environment as an opportunity to differentiate through quality. Schools that have maintained high standards now compete in a market with significantly reduced competitors willing to compromise on safety and preparation. Investment in instructor development, modern equipment, and comprehensive curricula becomes a competitive advantage.

The long-term effect should be an overall elevation in driver quality entering the market. Drivers trained under legitimized standards with qualified instructors are more likely to develop safer driving habits, demonstrate better hazard recognition, and show greater professional judgment. These qualities reduce accident rates, lower insurance costs for carriers, and improve safety for all road users. From a supply chain perspective, the slight near-term contraction in driver supply yields to long-term improvements in driver quality and reliability.

Practical Guidance for Freight Companies and Shippers

For companies that rely on trucking services, the transition period requires strategic planning. First, evaluate your current carrier relationships and driver availability. If your logistics depend on specific regional trucking capacity, assess whether that capacity is vulnerable to driver shortages in the transition period. Building relationships with multiple carriers provides flexibility if capacity constraints emerge.

Second, consider timing for major freight movements. If your company has flexibility in scheduling shipments, understanding regional driver supply dynamics helps optimize timing and reduce costs. Periods of acute driver shortage will correlate with higher rates and potentially longer delivery windows. Planning major shipments for periods of adequate driver availability can reduce logistics costs.

Third, work with your logistics partners to understand how they are managing driver supply and whether their operations might be affected by regional shortages. A quality 3PL or carrier should be proactively managing their driver workforce and communicating potential constraints. Companies that remain transparent about capacity and plan collaboratively with customers will be most valuable partners during this transition.

- Assess carrier capacity and regional driver availability

- Build relationships with multiple carriers for supply flexibility

- Time major shipments strategically to avoid high-constraint periods

- Work with logistics partners on capacity planning and communication

The Broader Lesson: Quality Standards in Regulated Industries

The CDL mill closure action offers a broader lesson about regulatory markets and infrastructure quality. When industries are regulated to protect public safety, enforcement of standards sometimes requires short-term capacity constraints. The government judged that maintaining driver quality was more important than maximizing the number of new drivers entering the market immediately. This represents a legitimate regulatory choice that prioritizes safety and long-term market health over short-term supply.

For supply chain professionals, this highlights the importance of understanding regulatory environments in the industries you depend on. Regulations exist for reasons, and enforcement actions, while sometimes disruptive, generally improve long-term outcomes. Companies that build supply chain strategies around regulatory compliance and quality providers rather than the cheapest alternative are more resilient when regulatory enforcement occurs.

The CDL mill closures will likely become a case study in how proper regulation of training and licensing can improve industry standards. As the driver market stabilizes with only quality training providers operating, metrics around safety, accident rates, and driver retention should improve. These improvements represent the true value of the regulatory action-a supply chain that is not only functioning but improving.

Looking Forward: Market Normalization and Recovery

The transition from the current state, where questionable training providers have been removed, to a normalized market with robust driver supply and elevated standards will take time. Realistic expectations for this period range from 18 to 36 months, depending on regional factors and the capacity expansion of legitimate training institutions.

During this period, companies should monitor driver availability trends, stay engaged with their logistics partners, and remain flexible in their supply chain planning. The temporary constraints are manageable for well-prepared companies but can surprise organizations that haven’t thought through the implications of the regulatory transition.

Ultimately, the trucking industry will emerge from this transition with higher-quality drivers, more professional training standards, and a supply chain that is both more regulated and more reliable. Companies that adapt to this transition thoughtfully will position themselves well for long-term logistics success.