How the Israeli attack on Iran is affecting and could further affect international trade in the region. This detailed exploration covers multiple trade segments, with an extended focus on energy trade and an in‐depth look at historical precedents where conflicts have reshaped trade patterns.

1. Overview and Immediate Impacts

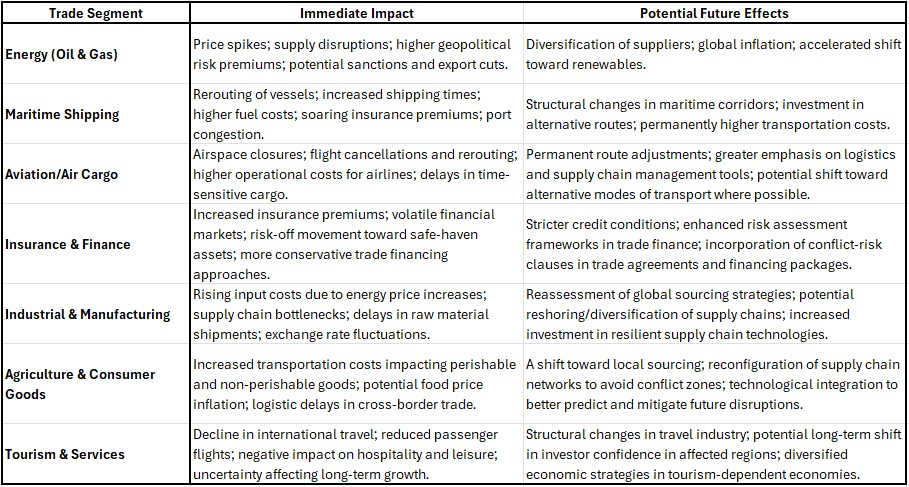

The attack has set off a chain reaction in global markets, destabilizing energy platforms, logistical networks, and financial systems. The initial shock was seen in abrupt spikes in crude oil prices, turbulence among shipping companies, a reordering of air cargo routes, and increased insurance premiums on high-risk shipments. These developments have led to rising operational costs and supply chain vulnerabilities, affecting trade not only in the Middle East but also globally. The heightened uncertainty is prompting governments and markets to reconsider security measures, diversify supply sources, and reinforce contingency planning—all while geopolitical alliances are being reshaped in real time.

2. Energy Trade Impact

Immediate Effects on Global Energy Markets

- Price Volatility: The attack has caused Brent crude and other benchmarks to surge by more than 10%, as traders factor in fears of disruption along key shipping lanes such as the Strait of Hormuz. Approximately 20% of global seaborne oil passes through this narrow passage, and any threat there can send global oil markets into a tailspin.

- Risk Premiums and Hedging: Investors have rushed into safe-haven assets like gold and U.S. Treasury bonds while energy futures are adjusted to incorporate geopolitical risk. Countries that heavily depend on Iranian oil are now reassessing their energy contracts and hedging strategies, driving a realignment of energy budget allocations.

- Supply Chain Uncertainty: Beyond immediate price hikes, there is a looming risk that any escalation will force countries to either impose new sanctions on Iran or preemptively substitute Iranian crude with alternative sources—a shift that may not come quickly due to infrastructure and contractual rigidity.

Longer-Term Ramifications

- Diversification of Energy Portfolios: Nations formerly dependent on Middle Eastern oil are accelerating efforts to secure alternative energy sources. This means a more rapid adoption of strategic reserves, investments in renewable energy projects, and forging new partnerships with other oil-producing nations. The persistent threat of disruption drives long-term policy adjustments geared toward energy security.

- Inflationary Pressures: As higher crude prices feed through to transportation, production, and ultimately consumer goods, inflation is set to rise globally. This inflation is not just an economic statistic—it directly affects cost structures across industries from manufacturing to agriculture.

- Geopolitical Realignments: Enhanced energy security concerns might compel some countries to reconsider their diplomatic ties. For instance, nations that previously maintained a balanced relationship with Iran might pivot more strongly toward partners like Saudi Arabia or Russia to secure a more stable energy supply chain.

3. Maritime Shipping and Logistics

Immediate Disruptions

- Rerouting and Increased Transit Times: The heightened risk in the Persian Gulf and the Strait of Hormuz forces shipping companies to look for alternative routes. These routes are longer, lead to increased fuel consumption, and add significant transit time—all culminating in higher shipping rates and delays.

- Insurance Premiums: Increased geopolitical risks translate into higher marine insurance costs, which are then passed on to importers and exporters. The imbalance adds pressure across all sectors that rely on maritime trade—from raw materials to finished consumer goods.

- Port Congestion: As vessels are rerouted or avoid high-risk ports, congestion builds at safer harbors. This increases turnaround times, disrupts inventory cycles, and ultimately affects broader industrial supply chains.

Strategic Considerations

- Infrastructure Investments: In response, some governments might invest in or expedite the development of alternative maritime corridors, potentially altering long-standing trade routes.

- Contingency Planning: Companies are increasingly forced to integrate risk mitigation into their logistics strategies—ranging from increased buffer stocks to investments in real-time route optimization technologies.

4. Aviation and Air Cargo Disruptions

Key Challenges

- Airspace Closures: With Iran, Israel, Iraq, and Jordan closing their airspace, both passenger and cargo flights are experiencing massive disruptions. This not only affects traveler mobility but also the timely delivery of high-value, time-sensitive goods such as pharmaceuticals and electronics.

- Increased Operational Costs: Rerouted flights incur additional fuel usage, extended operating hours, and higher maintenance costs. For industries operating on tight schedules, these delays can lead to significant disruptions in production and supply chain management.

- Ripple Effects on Logistics: The aviation sector, being a critical component of global supply chains, has seen a tightening of timing margins. This compels businesses to reexamine logistic contracts and integrate more robust alternative transportation modes where possible.

5. Insurance and Financial Markets

Immediate Market Reactions

- Increased Insurance Costs: With elevated risks across maritime, aviation, and even political domains, insurers have raised premiums steeply. This increase affects all trade segments and is a direct burden on operational costs for companies.

- Market Volatility: Global stock indices have reacted adversely, with futures trading down significantly. There is a noticeable shift away from risk assets into safer havens like government bonds and precious metals, further signaling market uncertainty.

- Conservative Trade Financing: Banks and financial institutions are likely to adopt more cautious lending practices amidst this uncertainty. Enhanced risk assessments will likely lead to new contract clauses that specifically address conflict-induced disruptions.

6. Industrial, Manufacturing, and Commodity Trade

Supply Chain Vulnerabilities

- Rising Input Costs: Industries face increased costs not only for energy but for raw materials whose prices are influenced by transportation delays and heightened insurance expenses. This affects manufacturing sectors—from automotive to electronics—by squeezing profit margins and increasing prices for end consumers.

- Production Bottlenecks: Disruptions in maritime and air cargo networks directly impede the timely delivery of components and raw materials. This forces many companies to either delay production or reconfigure supply chain networks, potentially even reshoring some manufacturing operations to mitigate long-term risks.

- Commodity Price Fluctuations: Agricultural, chemical, and metal commodities are also subject to price fluctuations due to the broader disruptions in supply routes and increased logistic expenses, potentially impacting global markets on a macroeconomic level.

7. Tourism and Service Trade

Sector-Specific Challenges

- Decline in International Travel: With airspace closures and heightened security concerns, tourism has taken a severe hit. This not only affects airlines but also impacts the hospitality, leisure, and local transportation sectors.

- Economic Downturn in Tourism-Dependent Economies: Regions that rely heavily on tourist inflow are expected to experience downturns. Reduced travel leads to diminished revenues in hotels, restaurants, and local attractions. The ripple effect may stretch to ancillary services including retail and entertainment.

- Long-Term Industry Adjustments: Prolonged instability could force governments to issue advisory warnings for travel, potentially restructuring the tourism sector and prompting economies to diversify their revenue streams away from an overreliance on tourism.

8. Geopolitical Trade Realignments

Strategic Shifts in International Relations

- Realignment of Diplomatic and Trade Ties: The conflict may push nations to recalibrate their strategic alliances. Countries forced to face high risks may pivot toward trade partners seen as more politically stable, even if this means breaking long-standing trade relationships.

- Incorporation of Conflict-Risk Clauses: Future international trade agreements and financing contracts may integrate explicit conflict-risk or force majeure clauses. This legal reconfiguration will likely influence how trade is negotiated and executed in conflict-prone regions.

- Emergence of New Trade Corridors: As traditional routes become riskier, governments and multinational entities might invest in developing new corridors. Whether through overland alternatives (such as rail networks) or enhanced maritime routes bypassing conflict hotspots, the landscape of global trade could be drastically redrawn.

9. Further Elaboration on the Energy Trade Segment

Given its centrality to both economic stability and geopolitical strategy, the energy trade segment warrants additional detailed exploration:

- Volume and Dependency Analysis: Iran is not only a significant medium for oil exports but also a key player in the global energy market due to its extensive natural gas reserves. Countries in Asia and Europe that rely on Iranian exports now face intensified pressures. A disruption in these volumes could compel importing nations to scramble for substitutes, thereby triggering global supply chain shocks.

- Futures Markets and Investor Behavior: The rapid uptick in oil futures has redefined market expectations. Investors are now pricing in a higher risk premium for oil, leading to increased volatility in commodities markets. This uncertainty forces countries to bolster their strategic petroleum reserves and reexamine long-term energy contracts. Futures contracts, which once traded on optimistic assumptions of uninterrupted flows, are now hedged extensively against possible shortages or rerouting delays.

- Diversification and Alternative Routes: The potential closure of the Strait of Hormuz underscores the vulnerability of single-route dependencies. Countries might invest in broadening their energy intake by:

- Policy and Regulatory Shifts: The conflict raises questions about how countries could use strategic reserves as both economic and political tools. In response, central banks and energy regulators might adjust policies to better manage future shocks, such as temporarily releasing reserves to stabilize markets or instituting emergency pricing regulations.

This extended examination of the energy trade segment reveals how a single geopolitical shock can trigger cascading effects that alter the entire global energy narrative—from futures markets to energy security policies.

10. Historical Perspectives: How Similar Conflicts Impacted Trade in the Past

Learning from history offers valuable insights into today’s dynamics:

- Iranian Revolution and Iran-Iraq War (1979–1988): The Iranian Revolution sharply disrupted oil supplies, and the ensuing Iran-Iraq War exacerbated the instability, leading to skyrocketing energy prices and forcing global traders to radically adjust their supply chains. These events illustrate how political upheaval can lead to long-term shifts in energy sourcing and pricing structures.

- The Gulf War (1990–1991): Iraq’s invasion of Kuwait and the subsequent conflict had a profound impact on international trade. The war led to a near-disruption of the oil trade through the Persian Gulf, heightened shipping risks, and caused insurance premiums to surge. Companies had to reroute their logistics and hedge aggressively against future uncertainties—a pattern echoed in today’s situation.

- Opium Wars and Colonial Trade Disruptions: Going further back, the 19th-century Opium Wars, though rooted in very different economic contexts, disrupted traditional trade routes and altered global trading power balances. The conflicts forced a reordering of international trade relationships that had long-term implications in establishing new economic corridors and legal frameworks to manage cross-border trade.

- Trade Wars of the Late 20th Century: More contemporary examples, such as the U.S.-China trade tensions, demonstrate how even non-military trade conflicts can lead to significant restructuring in global supply chains. Tariffs, currency manipulations, and targeted sanctions have historically led to market shifts, encouraging nations to diversify their trading partners and invest in strategic infrastructure.

Each of these historical episodes underscores a recurring theme: conflict—whether armed or economic—can catalyze rapid realignments in trade flows, force the diversification of suppliers, and redefine regional economic orders. Today’s Israel-Iran conflict fits into this broader historical pattern by not only immediately disrupting trade but also prompting a long-term reevaluation of energy policies and trade routes globally.

11. Concluding Thoughts

The Israeli attack on Iran is far more than an isolated military event—it is a catalyst for a broad, systemic reassessment of international trade networks. Energy markets are the most visible battleground; however, the ripple effects extend well into shipping, aviation, manufacturing, finance, and even tourism. The situation is dynamic, and while immediate disruptions have introduced heightened risk premiums and logistical delays, the long-term consequences may include profound shifts in geopolitical alliances, regulatory reforms, and strategic investments in alternative infrastructures.

By comparing today’s disruptions with historical cases—from the Iranian Revolution and Gulf War to the trade conflicts of earlier eras—we see clear patterns emerge. These patterns suggest that while trade networks are remarkably resilient, they are also perpetually vulnerable to shifts in political and military dynamics. In the coming months, as policymakers and market participants adapt to these changes, the international trade landscape could be reshaped to be more diversified, robust, and, ideally, less dependent on conflict-prone regions.