The Strait of Hormuz Crisis and Global Commodity Markets

Shipping disruptions in the Strait of Hormuz-one of the world’s most critical maritime chokepoints-have sent ripples through global commodity markets. The strait, through which roughly 21 percent of global petroleum trade flows, has become increasingly risky for vessel traffic due to geopolitical tensions in the region. These risks have particular implications for aluminum, where several major Middle Eastern smelters depend on strait transit for their exports.

In response to escalating security concerns, a number of major aluminum producers in the Gulf region have slowed shipments or temporarily halted exports. This supply response has driven aluminum prices higher on global exchanges, created uncertainty in physical delivery markets, and disrupted procurement timelines for manufacturers worldwide. The disruption demonstrates how regional geopolitical events can quickly cascade through integrated global commodity markets, affecting industries and countries far removed from the immediate crisis point.

Aluminum Supply Concentration and Market Structure

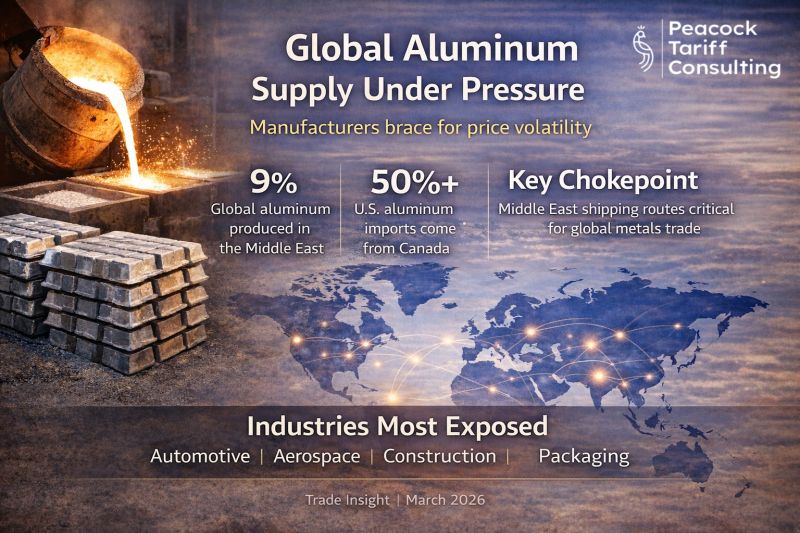

To understand the impact of Strait of Hormuz disruptions, it’s important to recognize the global structure of aluminum supply. Aluminum production requires massive capital investment in smelting facilities, access to reliable electrical power at competitive rates, and stable operating environments. These factors have created significant geographic concentration in production-with major smelting centers in the Middle East (particularly the Gulf states), Russia, Iceland, Canada, and China.

The Middle East has become an increasingly important aluminum producer due to access to cheap energy from oil and gas resources. Gulf-based smelters produce high-quality primary aluminum that supplies global markets. These facilities cannot easily reduce production and restart-aluminum smelting operates continuously, with significant warm-up periods if operations cease. This inflexibility means that when geopolitical risks make shipping through the strait dangerous, producers face difficult choices: continue operations and struggle to export, reduce operations and accept massive efficiency losses, or halt production entirely and face restart costs.

The result is that supply disruptions in the region tend to be sharp rather than gradual. A Middle Eastern producer cannot moderately reduce exports in response to ‘medium’ risk levels. Instead, they face binary choices that often lead to sudden supply curtailment when risks become unacceptable.

- Middle East smelters rely on cheap energy from oil and gas

- Aluminum production is capital-intensive and continuous

- Restarting smelters incurs significant efficiency penalties

- Supply decisions tend toward binary outcomes (on/off) rather than gradual adjustment

- Global aluminum market has concentrated production in a few regions

U.S. Aluminum Sourcing and North American Supply Security

A critical question for U.S. manufacturers: Does this crisis threaten American aluminum supply? The answer is largely reassuring, but with important caveats. The United States sources the majority of its aluminum imports from Canada, and Canada has a well-established, stable aluminum production infrastructure. Canadian smelters, powered by hydroelectric resources in British Columbia and Quebec, are geographically isolated from Middle Eastern supply chain risks and operate in a stable political and legal environment.

Beyond Canada, U.S. importers access aluminum from other global producers, including Scandinavia (powered by hydroelectric resources), Australia, and other sources. The North American market has deliberately cultivated supply diversity, making it more resilient to disruptions in any single source region. Unlike some commodities where geographic concentration creates severe vulnerability, aluminum sourcing patterns have provided U.S. manufacturers with meaningful supply security.

This does not mean, however, that the Strait of Hormuz crisis has no impact on North American manufacturers. Global commodity markets are integrated. When Middle Eastern supplies tighten, prices on the London Metal Exchange rise. These price increases are transmitted worldwide, affecting not just direct purchasers of Middle Eastern aluminum but all aluminum consumers as global pricing adjusts to reflect the reduced supply.

- Canada provides majority of U.S. aluminum imports

- Canadian supplies are geographically insulated from Middle East risks

- U.S. has diversified sources (Scandinavia, Australia, Russia)

- North American supply chains relatively stable despite global tightness

- Global price mechanisms still create exposure to supply shocks

Price and Market Impacts on Manufacturing

While North American physical aluminum supply remains relatively secure, manufacturers face real economic impacts. The first visible impact appears on the London Metal Exchange, where aluminum futures reflect global supply and demand. As Middle Eastern supplies tighten, global aluminum prices spike. These price increases immediately affect the economics of aluminum-intensive industries.

The second impact manifests in physical delivery premiums. Aluminum exists in multiple market tiers: the LME spot price (the theoretical price of standardized metal), the premium above the LME that reflects delivery logistics and supply tightness, and final delivered cost to manufacturers. When supply becomes uncertain, physical premiums increase. Sellers demand higher prices to compensate for the risk of being unable to deliver at contracted prices. Buyers accept higher premiums rather than face supply shortages. This premium compression into the supply chain increases effective material costs for manufacturers.

Beyond spot and premium prices, delivery timelines extend. Aluminum producers prioritize shipments to nearby markets and to customers with long-standing relationships. New orders or orders from distant markets face longer lead times as production is allocated to secure existing relationships. Manufacturers dependent on aluminum-particularly in automotive, aerospace, construction, and packaging-must adjust their own supply planning to accommodate longer lead times and accept the working capital impact of carrying larger inventory buffers.

- London Metal Exchange prices rise as global supply tightens

- Physical delivery premiums increase during supply disruptions

- Effective material costs rise beyond spot price increases

- Lead times extend as producers prioritize existing relationships

- Manufacturers build safety stock, increasing working capital needs

- Most-affected sectors: automotive, aerospace, construction, packaging

Industry-Specific Exposure and Response Strategies

Different manufacturing sectors experience the aluminum supply disruption with varying intensity. Automotive manufacturers-where aluminum usage has increased dramatically due to weight reduction goals-face significant exposure. Advanced aerospace manufacturers, where aluminum and aluminum alloys remain critical despite increasing use of composite materials, face both supply and cost pressure. The construction industry, which uses substantial volumes of aluminum for framing, roofing, and facade systems, experiences cost pressure that affects project economics. Packaging manufacturers, particularly those producing aluminum cans, have relatively less flexibility to substitute materials or reduce consumption.

Sector-specific response strategies vary accordingly. Automotive manufacturers with visibility into demand trends can increase aluminum alloy specifications in procurement, building purchases ahead of predicted price spikes-an option that requires working capital availability and demand certainty. Aerospace manufacturers often have long-term supply contracts with fixed pricing, meaning some are insulated from near-term price movements while others face significant margin pressure. Construction companies can temporarily shift project specifications to alternative materials, delay lower-priority projects, or increase bids to pass costs to customers.

For all sectors, the strategic response to commodity volatility involves several elements: visibility into total aluminum consumption across the supply chain, relationships with multiple suppliers that provide alternative sourcing, hedging strategies where cash flow and operations support financial hedging, and contingency plans for alternative materials where feasible. Companies that maintain these capabilities can navigate disruptions with limited operational impact, while those caught unprepared face margin compression or supply challenges.

- Automotive: high exposure, can pre-buy if demand visibility exists

- Aerospace: often protected by long-term contracts, but some face margin pressure

- Construction: can substitute materials or delay projects

- Packaging: limited substitution options, cost pressure flows through to consumers

- Hedging strategies provide financial protection where appropriate

- Supplier relationship diversity critical for access during disruptions

Longer-Term Supply Chain Resilience Considerations

The Strait of Hormuz disruptions, like other commodity supply shocks, provide useful signals for strategic supply chain design. Aluminum is not a material under structural shortage-global production capacity is adequate, and demand growth is moderate. Disruptions are therefore temporary, typically resolving within months as supply chains reorganize and producers shift distribution patterns. This near-term volatility, however, suggests valuable lessons about supply chain architecture.

Companies highly dependent on aluminum should evaluate their exposure to geographic concentration of supply, single-supplier dependency, and lack of inventory buffers. Some exposure to these vulnerabilities is inevitable given cost pressures in competitive manufacturing. But the optimal level of exposure is higher than pure cost minimization would suggest. Building modest supply chain redundancy-maintaining relationships with producers in multiple geographic regions, carrying strategic inventory for critical aluminum grades, qualifying secondary material specifications that substitute for primary choices-provides insurance against disruption at reasonable cost.

At the industry and policy level, these disruptions highlight why domestic or allied-source production capacity for critical materials matters. Countries and regions that are entirely dependent on imports for critical commodities face both economic and strategic vulnerability. Investment in North American aluminum production capacity, while not economically optimal from a pure cost perspective, provides value through supply security.

- Aluminum supply disruptions are typically temporary

- Build modest redundancy in geographic sourcing

- Maintain relationships with multiple regional producers

- Strategic inventory buffers protect against near-term volatility

- Qualify alternative material specifications to provide flexibility

- Domestic and allied-source capacity provides strategic value

Conclusion: Managing Commodity Risk in Connected Markets

The Strait of Hormuz aluminum disruption, while creating real economic headwinds, does not threaten North American physical supply. Canadian aluminum producers provide a stable, geographically secure supply source that insulates U.S. and North American manufacturers from Middle Eastern supply disruptions. This is an important distinction-one that many manufacturers understand clearly but that sometimes gets lost in headlines about global supply chain crisis.

That said, the disruption is not costless. Global commodity pricing, extended delivery timelines, and physical premium increases all affect the bottom line of aluminum-intensive manufacturers. Managing these impacts requires supply chain visibility, supplier relationship management, appropriate inventory buffering, and where feasible, material substitution strategies.

For supply chain professionals, the broader lesson is that geographic supply chain vulnerability varies by commodity, region, and supply chain structure. Blanket ‘nearshoring’ or ‘friendshoring’ strategies, while addressing important resilience concerns, may not match the actual risk profile of every commodity and every supply chain. Smart supply chain design involves differentiated strategies based on actual supply concentration risks, geopolitical exposure, and the economic cost of maintaining resilience. The aluminum market demonstrates that North American supply chain resilience, at least for this critical commodity, is already reasonably well designed.