The Tariff Tax on American Households

Recent analysis by the Tax Foundation reveals a concerning trend: tariffs are functioning as a hidden tax on American households, with measurable consequences for consumer debt levels. According to the Foundation’s research, the average American household absorbed approximately $1,000 in tariff-driven cost increases during the prior year, with projections suggesting that figure will climb to $1,300 in the current year. These are not abstract economic statistics-they represent real purchasing power erosion affecting family budgets across the income spectrum.

The tariff burden operates through mechanisms that are largely invisible to consumers at the point of purchase. When imported components become more expensive due to tariffs, manufacturers incorporate those costs into final product prices. Retailers pass those prices along to consumers. Tariffs on textiles raise clothing prices. Tariffs on electronics raise appliance and device costs. Tariffs on steel and aluminum increase prices for vehicles, tools, and construction materials. The cumulative effect is a widespread increase in the cost of everyday goods that households rely upon.

- Average household tariff burden: $1,000 in prior year

- Projected increase to $1,300 in current year

- Tariffs embedded in prices of clothing, appliances, vehicles, tools

- Cost increases distributed across all income levels

- Effects compound on households with multiple tariff-exposed purchases

The Debt Delinquency Connection

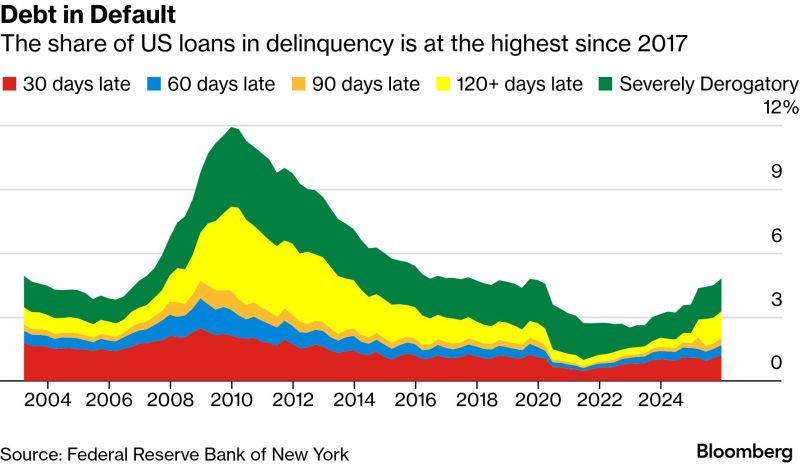

The correlation between tariff-driven inflation and household debt stress is not speculative. Credit card delinquency rates in Q4 2025 reached 4.8%, the highest level recorded since 2017. Simultaneously, other measures of household financial stress-late auto loan payments, mortgage delinquencies, and rising personal bankruptcies-have climbed from near-historic lows to elevated levels. Financial economists point to the timing alignment between tariff expansions and delinquency increases as evidence of causation rather than mere correlation.

The mechanism is straightforward. When household budgets are stretched by elevated prices for everyday goods, discretionary spending contracts first, but eventually the pressure extends into essential spending categories. Households begin stretching payments, missing due dates, and ultimately defaulting on obligations. This pattern emerged clearly in 2025 as tariffs expanded and cost of living pressures intensified. The delinquency data reflects millions of households deciding they can no longer afford their current payment obligations.

- Credit card delinquency rate: 4.8% in Q4 2025

- Highest delinquency rate since 2017

- Aligned timing with tariff expansions

- Auto loan and mortgage delinquencies also elevated

- Personal bankruptcy filings increasing

Tariff Impacts Across the Consumption Basket

Tariffs affect different product categories with varying intensity, meaning that the burden falls unevenly across household budgets. Categories with particularly high tariff exposure include apparel and footwear (average duties 15-25%), consumer electronics (10-25%), furniture and home goods (10-20%), and vehicles (2.5%, but concentrated on imported models). For households heavily dependent on these categories-families with children requiring frequent clothing replacement, low-income households stretched across multiple categories, and rural households relying on vehicle transportation-the tariff burden is disproportionately severe.

Additionally, tariffs create cascading effects through supply chains. A tariff on imported steel increases the cost of automobiles, appliances, tools, and construction materials simultaneously. A company paying higher tariff costs for imported inputs may reduce employment, lowering wages in communities dependent on manufacturing. The indirect effects ripple through local economies in ways that extend beyond the direct price increases visible to consumers.

- Apparel/footwear: 15-25% average duties

- Consumer electronics: 10-25% duties

- Furniture and home goods: 10-20% duties

- Imported vehicles face 2.5% base duty plus tariffs on components

- Tariff cascades through supply chains affect multiple product categories

The Policy Design Problem

From a macroeconomic perspective, the tariff-driven household debt increase reflects a fundamental design problem in how tariffs are structured and communicated. Tariffs are ostensibly imposed to protect American manufacturing or serve other trade policy objectives, yet the policy instruments are blunt. They raise prices broadly across consumption categories without distinguishing between households by income level or necessity of the tariffed goods.

This stands in sharp contrast to other forms of consumer cost imposition that are explicitly designed with progressive structures. Income taxes scale with earnings capacity. Sales taxes often exempt necessities. Utility rates may include protections for low-income consumers. Tariffs, by contrast, impose identical tax burdens on wealthy and poor households alike, making them regressive by definition. A family earning $35,000 annually bears the same tariff cost increase as a family earning $150,000, despite vastly different capacity to absorb cost increases.

- Tariffs impose uniform burden regardless of household income

- Regressive policy structure affects low-income households disproportionately

- No exemptions for necessities or vulnerable populations

- Broader than typical tax structures in incidence

- Policy design ignores distributional consequences

Long-Term Household Financial Stress

The immediate impact of elevated household debt is elevated financial stress and reduced access to credit. As delinquency rates rise, credit card companies increase interest rates, making borrowing more expensive for those who need credit most. Mortgage lenders tighten standards, making homeownership less accessible. The virtuous cycle of broad-based consumer access to credit contracts into a vicious cycle where financial stress concentrates in vulnerable populations.

Over longer horizons, elevated household debt burdens reduce consumer purchasing power for discretionary goods and services, dampening economic growth. Households stretched financially reduce spending on dining out, entertainment, travel, and other discretionary categories. Small businesses dependent on discretionary consumer spending experience demand contraction. This can trigger business failures, employment losses, and further compression of household incomes. The tariff-driven cost increases, while initially appearing localized to specific product categories, can cascade into broader economic contraction if the scale of household financial stress becomes severe enough.

- Rising delinquency reduces credit access and availability

- Interest rates increase for credit-dependent consumers

- Mortgage lending standards tighten

- Household debt stress reduces discretionary spending

- Small businesses dependent on discretionary spending experience demand contraction

Policy Options and Considerations

Policymakers face difficult choices regarding tariff policy. The stated objectives-protecting domestic manufacturing, addressing trade imbalances, supporting worker communities-are legitimate concerns that resonate with many constituencies. However, the evidence increasingly shows that broad-based tariffs impose substantial costs on households that may not be offset by the policy’s intended benefits in ways that affect those same households.

Some policy analysts suggest targeted approaches that maintain tariff protection in specific sectors while exempting goods essential to household consumption. Others advocate for complementary policies like direct cash transfers to affected households or targeted tax credits for low-income consumers. Still others argue that tariff costs should be offset through reductions in other taxes, explicitly rebalancing the burden. These alternatives all recognize that effective trade policy requires not just setting tariff levels, but managing the distributional consequences for households across income levels.

- Tariffs serve legitimate policy objectives but with household cost implications

- Targeted approaches could maintain protection while limiting consumer impact

- Direct household assistance could offset tariff burden regressive effects

- Tax rebalancing could distribute tariff costs more fairly

- Policy design requires attention to distributional consequences