The First Sale Doctrine Under Legislative Siege

Senators Cassidy and Whitehouse have introduced the Last Sale Valuation Act, legislation that would fundamentally restructure how U.S. Customs calculates duties on imported goods. The act would eliminate the First Sale Doctrine, which allows companies to calculate duties based on the price at which a foreign manufacturer sells goods to an export intermediary, rather than the final price at which those goods are sold to the U.S. importer. If enacted, this legislation would force duty calculation on the final sale price to the U.S. importer-a change that would increase duty costs across almost every imported product category.

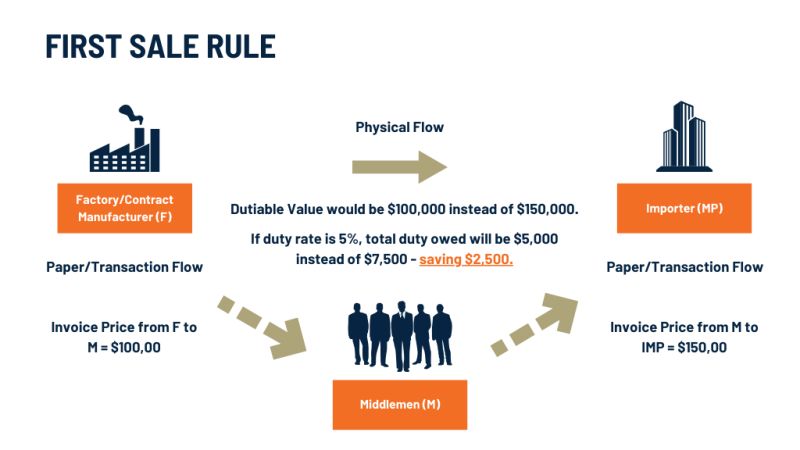

The First Sale Doctrine has been a cornerstone of U.S. customs valuation law for decades. It reflects the principle that the value at which a product is valued for duty purposes should be the price at which the exporting company sells the product, not the price at which intermediaries or final buyers subsequently purchase it. Eliminating this doctrine represents a frontal assault on a valuation principle that has shaped international trade and supply chain structures for generations.

- Senators Cassidy and Whitehouse introduced Last Sale Valuation Act

- Would eliminate First Sale Doctrine in duty calculation

- Duties would be based on final sale price to U.S. importer

- Represents fundamental restructuring of customs valuation

- Affects duties across virtually all import categories

Valuation Impact and Duty Increase Calculations

The magnitude of duty increase from Last Sale Valuation depends on the markup between the export sale price and final import price. For many products, intermediaries and logistics operators add 20-40% markup between the export transaction and the point at which goods arrive at the U.S. importer. Apparel manufactured in Bangladesh at an export price of $5 per unit might have a $2-3 per unit markup by the time it reaches the U.S. retailer, making the final sale price $7-8 per unit. Under current law, duties are calculated on the $5 export price; under Last Sale Valuation, duties would be calculated on the $7-8 final price, increasing duty burden by 40-60%.

For companies operating international supply chains, this is not an abstract calculation. A company importing $100 million in goods annually at an average 15% tariff rate currently pays $15 million in duties. If Last Sale Valuation increases the valuation base by 30% due to supply chain markups, duty costs rise to approximately $19.5 million-a $4.5 million annual increase. For companies with thin margins, this increase is material enough to affect profitability and competitiveness. Multiply across all U.S. importers and the aggregate duty revenue impact exceeds tens of billions of dollars annually.

- Export sale price typically 20-40% below final import price

- Duty increases calculated on full final price markup

- Example: 15% duties on $100M imports rise $4.5M with 30% markup increase

- Aggregate duty impact across all importers: tens of billions annually

- Material impact on company profitability and competitiveness

Industries Most Heavily Affected

The Last Sale Valuation Act would disproportionately affect industries characterized by extended supply chains with multiple intermediaries between manufacturer and importer. Apparel and footwear, where goods typically move from factory to consolidator to freight forwarder to U.S. warehouse to retailer, faces substantial duty increases. Consumer goods, electronics, toys, and furniture-all products typically distributed through intermediaries-face similar exposure.

Pharmaceutical and medical device industries would also be heavily affected, despite their reputation as higher-margin, lower-volume categories. Many pharmaceuticals move through distributors, wholesalers, and logistics operators that add layers of markup. The increased duty burden on pharmaceuticals could affect medication costs and healthcare economics. Automotive components, while often distributed directly, still frequently move through intermediaries, creating exposure. Chemicals and basic materials, distributed through traders and consolidators, also face valuation increases. Very few import categories escape the exposure.

- Apparel and footwear: extended supply chains with multiple intermediaries

- Consumer goods, electronics, toys, furniture: significant exposure

- Pharmaceuticals and medical devices: cost impacts on healthcare

- Automotive components: distributed through intermediaries

- Chemicals and materials: traded through consolidators and traders

Supply Chain Restructuring Implications

The Last Sale Valuation Act would create powerful economic incentives for supply chain restructuring. Currently, companies benefit from supply chain architecture that includes consolidators, traders, and logistics operators who add value through aggregation, storage, customs clearance, and distribution services. Under Last Sale Valuation, these intermediaries’ markups become duty-taxable, making the supply chain architecture more expensive.

Companies would face incentive to restructure supply chains to eliminate intermediaries where possible. Direct purchasing from manufacturers, vertical integration into distribution, or consolidated logistics arrangements would all become more valuable by reducing the valuation markup subject to duty. This could trigger consolidation in logistics and trading industries, as companies attempt to internalize functions previously handled by intermediaries. Small companies that depend on intermediaries for supply chain functions may find that the duty cost increase makes direct supply chain management infeasible, limiting their ability to import.

- Current supply chain intermediaries add markup subject to future duty taxation

- Supply chain restructuring incentives: eliminate intermediaries

- Direct purchasing from manufacturers becomes more valuable

- Vertical integration into distribution becomes more economical

- Consolidated logistics arrangements reduce duty valuation exposure

Transfer Pricing and International Tax Implications

The Last Sale Valuation Act intersects with transfer pricing rules that govern how multinational companies allocate income and costs across countries. Many multinational companies structure their supply chains to set transfer prices at levels that optimize both tariff duties and corporate income taxes. Eliminating the First Sale Doctrine would disrupt these optimized structures and create conflicts between tariff duty minimization and transfer pricing tax optimization.

For multinational companies with integrated supply chains, this creates potential double taxation or penalty situations. A company that minimized tariff duties through strategic transfer pricing might now find that transfer pricing optimizations are incompatible with Last Sale Valuation requirements. This could trigger disputes with both customs authorities (over valuation) and tax authorities (over transfer pricing). The interplay between tariff valuation law and transfer pricing tax law, historically managed through careful supply chain structuring, would become more fraught and contentious. Companies operating multinational supply chains would need to recalibrate their entire structure to optimize across both tariff and tax considerations simultaneously.

- Transfer pricing structures designed to optimize both tariffs and income taxes

- Last Sale Valuation disrupts historically optimized supply chains

- Potential conflicts between tariff minimization and transfer pricing optimization

- Risk of disputes with both customs and tax authorities

- Double taxation exposure for multinational companies

Congressional Motivation and Political Context

The legislative motivation behind the Last Sale Valuation Act reflects political concern that current valuation rules allow companies to avoid duty responsibility through supply chain architecture. From a congressional perspective, companies are using intermediaries and supply chain markups to reduce the valuation base for duties, thereby reducing duty revenues and, implicitly, undercutting tariff policy objectives. By forcing duties to be calculated on final sale prices, Congress intends to increase duty revenue and prevent what it views as tariff avoidance through supply chain engineering.

The act also reflects a protectionist impulse to increase the effective tariff burden on imports, making domestic products relatively more competitive. By increasing duty costs, Congress intends to reduce import competitiveness and support domestic suppliers. The legislation positions itself as tariff policy enforcement, preventing companies from circumventing tariff protection through valuation manipulation. Whether the act is accurate in this characterization-whether current supply chains actually constitute tariff avoidance rather than efficient logistics-is contested. But the political motivation is clear: increase effective duties by expanding the valuation base.

- Political concern about tariff avoidance through supply chain architecture

- Intent to increase duty revenue through expanded valuation base

- Protectionist objective: increase import costs, support domestic suppliers

- Positions act as tariff enforcement rather than new tariff imposition

- Contested whether current practices constitute avoidance or efficient logistics

Recommendations for Importers and Supply Chain Operators

If the Last Sale Valuation Act advances toward enactment, importers face a critical period in which to evaluate and potentially restructure their supply chains. Begin immediately with a comprehensive valuation audit. For each product line, calculate current valuation bases, identify all intermediaries and markups between manufacturer and importer, and model how Last Sale Valuation would change duty costs. This analysis should reveal which product lines face the greatest duty increase exposure.

Second, evaluate supply chain restructuring options. Could you source directly from manufacturers and eliminate consolidators? Could you integrate logistics or customs clearance functions in-house? Could you partner with multinational freight forwarders that could operate on lower markup percentages? Could you negotiate direct pricing with manufacturers that incorporates supply chain functions currently handled by intermediaries? Each option has different implications for supply chain risk, cash flow management, and operational complexity, but the duty savings might justify restructuring.

Third, engage with industry associations and congressional representatives to express the business impact of Last Sale Valuation. Supply chain operators, intermediaries, and importers should communicate to Congress the potential consequences for supply chain efficiency, employment, and costs. If the act is controversial enough, it might stall in Congress. If it appears likely to pass, supply chain restructuring becomes a more urgent priority. Finally, consult with tariff professionals to understand the implications for your specific supply chains and develop contingency plans for valuation changes.

- Conduct comprehensive valuation audit of all product lines

- Calculate current valuation bases and intermediary markups

- Model duty cost impacts of Last Sale Valuation

- Evaluate supply chain restructuring options

- Consider direct sourcing from manufacturers

- Negotiate integrated pricing with manufacturers

- Engage with industry associations for congressional advocacy

- Consult tariff professionals on valuation implications