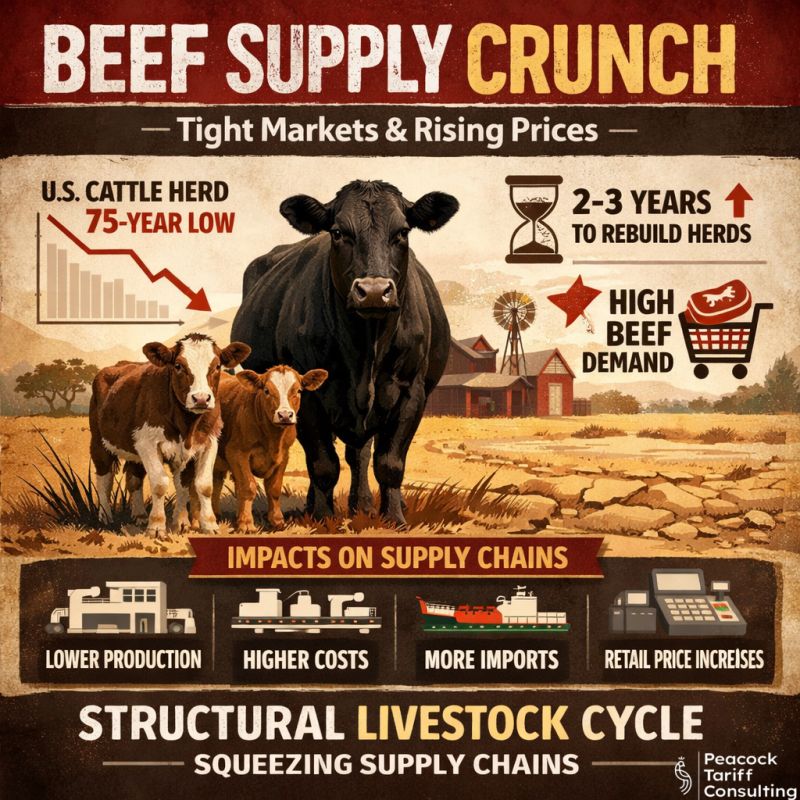

The Severity of the Crisis: A 75-Year Low

The U.S. cattle herd has reached its lowest level since 1951-a startling statistic that signals far more than a temporary market fluctuation. This decline represents a fundamental disruption in one of America’s most essential agricultural supply chains. Retail beef prices have already surged approximately 17 percent year-over-year across North America, and industry analysts warn that this pressure may persist for years to come, not months.

The numbers tell the story of structural strain. Years of sustained drought have devastated grazing lands across the Great Plains and Western states. Feed costs have climbed to historically elevated levels, making the economics of cattle ranching increasingly challenging. Faced with these pressures, ranchers have made deliberate decisions to reduce herd sizes-decisions that have cascading consequences throughout the entire protein supply chain. When ranchers reduce cattle populations, they are not responding to temporary market signals; they are making structural adjustments that reshape supply patterns for years.

The Biological Production Cycle: Why Recovery Takes Years, Not Months

Understanding why this crisis will persist requires grasping a fundamental reality of livestock agriculture: the biological production cycle. Unlike manufactured goods that can be produced quickly once orders increase, cattle require time to mature and reproduce. A cow pregnancy lasts approximately nine months. Calves must then be raised and fattened before they can be processed. If a rancher decides today to expand their herd, the impact on beef supply will not materialize for two to three years.

This biological lag means that even if market conditions were to dramatically improve tomorrow, U.S. beef supply would remain constrained through 2028 or beyond. The industry is caught in what economists call a ‘cobweb cycle’-prices rise due to scarcity, but high prices alone cannot immediately expand supply. Instead, ranchers make breeding decisions based on current economic conditions, and those decisions play out over years. This structural dynamic is why supply chain managers cannot treat the current cattle shortage as a temporary disruption but rather as a multi-year headwind.

Upstream Pressures: How Cattle Shortage Ripples Through the Supply Chain

The impact of reduced cattle supplies does not remain confined to ranching operations. Instead, it propagates upstream through processing, distribution, retail, and food service. Beef processors-the companies that slaughter and process cattle into consumer-ready products-are operating plants below capacity because there are simply fewer cattle available for processing. This inefficiency raises per-unit production costs, which are then passed downstream.

Retail grocers are facing a stark choice: either absorb lower margins by maintaining competitive pricing or pass cost increases to consumers. Most are choosing the latter, which is why shoppers are seeing the 17 percent price increases at checkout. Food service establishments-restaurants, hotels, and institutional food services-face similar pressures. Premium beef cuts are becoming scarcer and more expensive, forcing menu adjustments and pricing changes that consumers experience when they dine out.

The supply constraint is bidirectional. Because U.S. beef production is expected to remain constrained, some food companies and retailers are increasing imports of beef from countries such as Brazil, Argentina, and Australia. While imports help stabilize overall supply, they increase costs due to shipping, tariffs, and exchange rate fluctuations. They also reduce the economic benefit to U.S. ranchers and beef processors, creating a secondary effect of further pressure on domestic production economics.

Demand Resilience: Why Prices Cannot Fall Back to Normal Levels

In a typical supply shortage, high prices eventually suppress demand, allowing supply and demand to rebalance at a lower quantity and higher price. However, beef demand has proven remarkably resilient despite price increases. This resilience reflects several factors: beef remains a preferred protein for many consumers despite higher costs; dietary preferences continue to favor animal proteins; and institutional buyers (restaurants, food service) cannot easily switch away from beef without altering their menus and offerings.

This demand resilience is unusual and consequential. It means that high beef prices are unlikely to create sufficient demand destruction to clear markets. Instead, prices will likely remain elevated for years as the industry gradually rebuilds cattle herds. Supply chain managers cannot assume that demand-side adjustment will relieve the pressure they are experiencing.

Supply Chain Adaptation Strategies

For companies operating within the beef supply chain, adaptation is essential. Food manufacturers and retailers should consider diversifying their protein sourcing strategies. This might include increasing the proportion of alternative proteins (chicken, pork, plant-based options) in their product mix, sourcing more beef imports, or adjusting product formulations to use less beef per unit.

Food service operators should evaluate menu pricing, portion sizes, and product mix. Some establishments may find opportunities in offering smaller, premium-priced beef servings rather than attempting to maintain traditional portion sizes at traditional price points. Others may develop value-oriented alternatives that shift customers toward lower-cost proteins when beef is unavailable at acceptable prices.

For beef processors and distributors, investing in operational efficiency and cost reduction is critical. The longer the supply shortage persists, the more important it becomes to maintain market share through operational excellence rather than relying on high prices to sustain margins. Companies should also explore value-added processing-premium cuts, specialty products, and niche market offerings-that capture higher margins than commodity beef.

Supply chain professionals should also begin scenario planning around extended periods of high beef prices. If herd rebuilding takes longer than expected due to continued drought or other challenges, beef scarcity could persist into 2029 or beyond. Building resilience into supply chains now will protect profitability during extended periods of constraint.

Long-Term Structural Factors: This Is Not Short-Term Inflation

It is tempting to interpret the current beef shortage as a temporary inflation story that will reverse once supply catches up or demand weakens. This interpretation would be dangerously incorrect. The current situation reflects structural challenges in U.S. agriculture that are not readily reversible. Climate patterns, including sustained drought in key cattle-producing regions, may represent a ‘new normal’ rather than a temporary fluctuation. Water availability, which drives forage production and ranching economics, will remain constrained in Western states regardless of near-term weather patterns.

Additionally, the economics of cattle ranching have shifted. Feed costs have risen due to global agricultural dynamics, energy prices, and input inflation. These cost pressures are unlikely to reverse dramatically. Ranchers making herd reduction decisions are responding rationally to these economic fundamentals. Even as cattle prices rise, the margin between revenues and costs may remain too thin to incentivize rapid herd expansion.

For supply chain managers, this analysis has profound implications. Beef prices are unlikely to return to their 2019-2020 levels. Instead, the industry is transitioning to a ‘new normal’ characterized by smaller herds, tighter supplies, and higher prices. Supply chains must be designed for this permanent reality, not built around an assumption of future price normalization.

Conclusion: Preparing for Years of Protein Scarcity

The U.S. cattle herd decline to a 75-year low is not a temporary market disturbance but a structural challenge that will reshape protein supply chains for years. The biological production cycle ensures that herd recovery will take time. Demand resilience ensures that prices will remain elevated. And underlying economic and climatic factors ensure that ranchers will remain cautious about rapid expansion.

For supply chain managers, food manufacturers, retailers, and food service operators, the imperative is clear: treat this as a structural, multi-year challenge rather than a cyclical disruption. Diversify protein sourcing, adjust pricing and product strategies, invest in operational efficiency, and build supply chain resilience around the reality of sustained beef scarcity. By taking these steps now, companies can navigate the coming years of protein constraints and position themselves for success when the market eventually stabilizes at a new, higher-price equilibrium.