Storage Capacity Filling Rapidly: A Critical Constraint

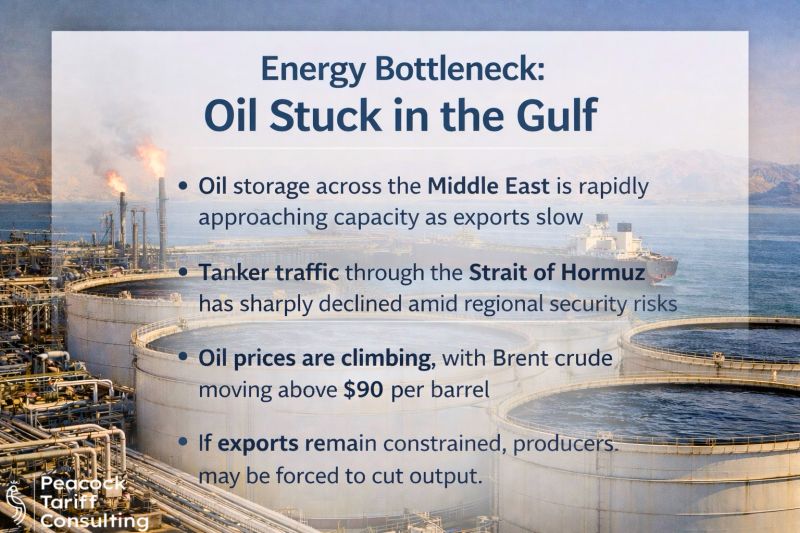

Oil storage facilities in the Middle East are filling rapidly, reaching capacity limits that constrain production flexibility and signal growing imbalances in global oil markets. When storage facilities reach capacity, producers face difficult choices: they cannot continue production at current levels without somewhere to store the oil, existing storage capacity must be released, or production must be cut. The rapid filling of Middle East storage indicates that oil production currently exceeds export capacity, creating a supply-demand imbalance that forces operational decisions.

The oil storage constraint is particularly significant because the Middle East represents one-quarter of global oil production. Saudi Arabia, Iraq, United Arab Emirates, Kuwait, and Iran collectively produce approximately 25 million barrels per day, representing roughly 25% of global production. When storage facilities in this region fill, the constraint affects global oil markets immediately. Unlike some supply constraints that affect regional markets, Middle East storage constraints ripple through global supply chains because Middle East production has global significance.

- Middle East oil storage facilities reaching capacity

- Production exceeding export capacity creating supply-demand imbalance

- Constraint affecting region producing 25% of global oil

- Rapid filling indicating structural supply-demand mismatch

Tanker Traffic Disruption and Transportation Bottlenecks

Tanker traffic through the Strait of Hormuz, the critical chokepoint for Middle East oil exports, faces heavy disruption. The strait normally handles approximately 21 million barrels per day of crude oil and products, representing roughly 21% of global seaborne oil trade. When tanker traffic is heavily disrupted, oil exports from the Middle East are constrained regardless of production capacity. This combination of high storage levels and transportation disruptions creates a supply squeeze where oil cannot easily exit the region.

The transportation disruption compounds the storage problem. Oil accumulated in storage facilities would normally be exported via tankers, but if tanker traffic is disrupted, export capacity becomes severely constrained. This creates a circular problem: oil cannot be exported due to transportation constraints, so storage facilities fill; as storage facilities fill, producers face pressure to reduce production. The transportation disruption therefore directly constrains production flexibility by preventing export of stored oil.

- Strait of Hormuz tanker traffic heavily disrupted

- Strait normally handles 21 million barrels per day

- Disruption preventing export of accumulated oil

- Storage and transportation constraints combining restrictively

Production Decision Framework: Cut, Shut-In, or Alternative Routes

When storage is full and transportation is disrupted, oil producers face three options: reduce production to match constrained export capacity, shut in wells to preserve oil for future export, or find alternative export routes. Each option carries different costs and implications. Reducing production is economically painful because fixed production costs remain constant while revenue declines. Shutting in wells preserves flexibility but reduces current revenue. Alternative routes, if available, require redirecting oil through overland pipelines or other maritime routes that may be more expensive or lengthy.

The strategic choice producers make depends on price expectations, storage constraints, and financing requirements. If producers expect prices to rise substantially, they have incentive to preserve oil by reducing production rather than selling at current prices. If producers need current revenue, they may reduce production modestly while seeking alternative export routes. The Middle East storage filling is forcing producers to make these trade-offs explicitly. Some producers may shut in production; others may reduce output modestly; still others may seek alternative arrangements. The aggregate outcome is production constraint.

- Production reduction, well shut-in, or alternative routing options

- Each option carries distinct economic implications

- Price expectations affecting producer decisions

- Revenue requirements creating downward production pressure

Oil Price Support and Commodity Market Effects

The storage constraint, transportation disruption, and potential production cuts are supporting oil prices toward the $90 per barrel level. Supply constraints provide price support in commodity markets. When oil supply is constrained by storage and transportation limitations, prices strengthen. The $90 per barrel level reflects supply-demand tightness where constrained supply drives price increases. This price support persists as long as supply constraints remain.

The upward price movement creates a secondary effect: higher oil prices reduce consumption as customers seek conservation or alternative energy sources. Reduced consumption at higher prices creates demand destruction that eventually balances supply constraints. However, the immediate market dynamic features supply-constrained pricing at elevated levels. The $90 per barrel level is not a temporary spike but reflects structural constraint of supply relative to normal export capacity.

- Oil prices pushed toward $90 per barrel

- Supply constraints providing price support

- Higher prices reducing consumption through demand destruction

- Elevated price levels persisting while constraints remain

Downstream Supply Chain Impacts: Plastics, Chemicals, Fertilizers

Oil is the feedstock for far more than transportation fuel; it is the raw material for plastics, chemicals, fertilizers, and countless industrial products. When oil prices rise to $90 per barrel, the cost of these downstream products increases correspondingly. Plastics manufacturers face higher raw material costs and increase product pricing. Chemical manufacturers that depend on crude oil derivatives face cost increases that flow through to final products. Fertilizer manufacturers that use petrochemical inputs face elevated input costs. These downstream supply chain impacts spread oil price pressures throughout manufacturing and agriculture.

The broader economic impact of elevated oil prices extends beyond direct energy costs to encompass multiple industries dependent on oil-based feedstocks. Automotive manufacturers purchasing plastic components face higher input costs. Electronics manufacturers using plastic housings and chemical coatings face cost increases. Agricultural producers using fertilizer and diesel fuel face compound cost increases. The multiplier effects of elevated oil prices ripple through supply chains, creating cost inflation across diverse industries. These cascading costs ultimately reach consumers through higher product prices.

- Plastics, chemicals, fertilizers all dependent on oil feedstock

- Oil cost increases flowing through to product costs

- Automotive, electronics, agriculture facing cascading cost pressures

- Consumer price inflation from oil-dependent supply chains

Transportation and Manufacturing Cost Inflation

Oil price pressure directly affects transportation costs through fuel prices. Higher oil prices mean higher diesel and jet fuel costs, which increase costs for trucking, ocean shipping, rail transport, and air freight. Transportation cost increases affect all goods that require transportation, creating economy-wide cost inflation. Manufacturing costs increase as both inputs and distribution costs rise. Global supply chains relying on transportation become more expensive to operate, creating incentives to shorten supply chains or accept delivery delays.

The transportation cost component of the oil price shock is immediate and measurable. Container shipping rates, trucking rates, and logistics costs all increase when fuel costs rise. These cost increases affect import prices, export competitiveness, and internal distribution costs. The cumulative effect of transportation cost increases compounds other oil-related cost pressures, creating multi-layered cost inflation affecting manufacturing and retail.

- Diesel costs increasing with oil prices affecting transportation

- Container shipping rates rising with fuel costs

- Trucking and logistics costs increasing across supply chains

- Transportation inflation affecting import and export pricing

Market Outlook and Resolution Scenarios

The Middle East oil storage crisis and transportation disruptions will persist until either storage capacity is relieved or additional export capacity is developed. If storage fills to capacity and remains full, producers must reduce production or shut in wells, creating sustained production constraint. If transportation disruptions resolve, tanker traffic normalizes, and storage can be drawn down. The resolution of the storage crisis depends primarily on whether Strait of Hormuz disruptions persist or are resolved.

Short-term outlook suggests continued oil market tightness. Storage continues filling, transportation remains disrupted, and producers continue facing capacity constraints. Oil prices likely remain elevated near $90 per barrel or higher. If disruptions persist beyond Q2 2026, secondary storage constraints may develop in other regions, extending tightness. If disruptions resolve in Q2, storage can be drawn down through elevated export volumes, relieving constraints. The timing of disruption resolution is the critical variable determining when market conditions normalize.

- Storage capacity constraint persisting until disruption resolution

- Oil prices expected to remain elevated Q1-Q2 2026

- Secondary constraint development possible if disruptions persist

- Market normalization dependent on transportation recovery