The Current Crisis: MSC’s Emergency Fuel Surcharge Announcement

On March 16, 2026, Mediterranean Shipping Company (MSC), the world’s largest container carrier by fleet size, announced significant emergency fuel surcharges across multiple critical trade lanes. This decisive move reflects the cumulative impact of rising bunker fuel prices driven by ongoing geopolitical instability in the Middle East and operational challenges that force carriers to extend voyage distances through alternative routes.

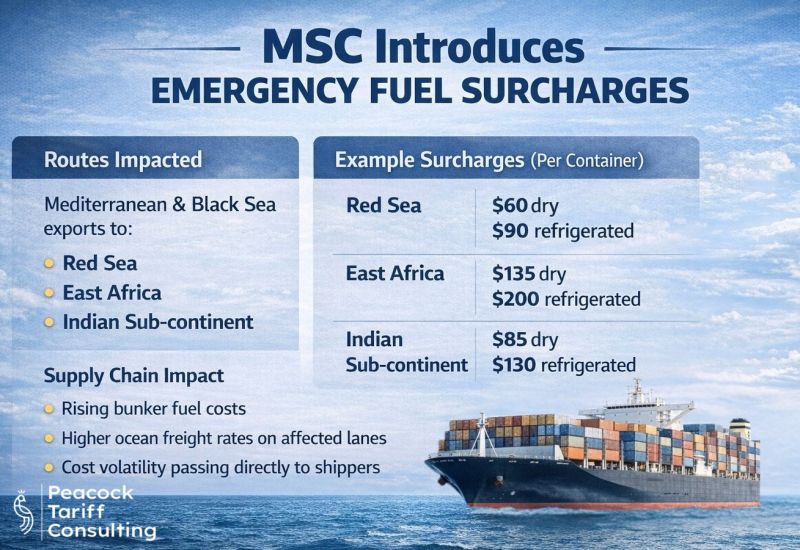

The surcharge structure is tiered by container type and trade lane, demonstrating how different routes face proportional cost pressures. From the Mediterranean to the Red Sea, carriers now charge $60 per dry container and $90 per refrigerated unit. The Mediterranean to East Africa route carries the highest surcharge at $135 for dry containers and $200 for refrigerated cargo. Mediterranean to Indian sub-continent routes fall in the middle at $85 and $130 respectively.

These increases are not arbitrary. They represent a direct pass-through mechanism from bunker fuel markets to shippers, revealing how energy market volatility now flows rapidly through global supply chains. For logistics managers and procurement professionals, understanding the mechanics behind these surcharges is essential for cost forecasting and budget planning.

- Emergency surcharges effective March 16, 2026

- Surcharges vary by destination and container type

- Direct correlation with bunker fuel price fluctuations

- MSC leading the industry in transparent price communication

The Root Cause: Bunker Fuel Volatility and Geopolitical Disruption

The immediate trigger for MSC’s surcharge announcement is the sharp increase in bunker fuel prices. Bunker fuel costs have surged due to two interconnected factors: first, geopolitical instability in the Middle East, which affects oil production and refining capacity; second, longer voyage distances that result from rerouting around established shipping choke points and conflict zones.

Shipping companies operate on remarkably thin margins, typically between 2-4 percent in competitive container markets. When fuel costs spike, carriers have limited options. They can absorb costs through reduced profit margins, implement immediate surcharges, or reduce capacity. Most major carriers choose a combination of approaches, with fuel surcharges providing the most transparent mechanism.

The longer routes now required for many Asian exports to Europe and Mediterranean destinations create compounding fuel consumption. A standard Asia-to-Europe service via the Suez Canal previously operated on relatively predictable fuel costs. Extended rerouting around the Cape of Good Hope or through alternative passages increases sailing distances by 4,000 to 6,000 nautical miles per voyage, multiplying fuel expenditures significantly across a year’s worth of sailings.

- Bunker fuel prices driven by Middle East geopolitical risks

- Extended voyage distances increase fuel consumption 15-30 percent

- Carrier profit margins compress to 2-4 percent under normal conditions

- Fuel surcharges essential to maintain vessel operations and capital reinvestment

Impact by Trade Lane: East Africa, Red Sea, and Indian Ocean Routes Face Greatest Pressure

Not all trade lanes face equal pressure. The surcharge amounts published by MSC reveal geographic differentials based on fuel consumption, distance traveled, and geopolitical risk factors. The highest surcharges apply to East Africa routes, reflecting both distance and instability in the region. Red Sea routes face significant surcharges due to ongoing security concerns that necessitate armed escort services and extended routing patterns.

For Indian sub-continent logistics, these surcharges represent a substantial cost increase. Shippers moving electronics, machinery, or raw materials to or from India now face additional margin pressure. The Indian sub-continent routes, historically among Asia’s most cost-competitive options, are becoming comparatively more expensive as fuel surcharges erode the cost advantage that attracted supply chain investment to these regions.

East African trade routes, increasingly important for sourcing raw materials and agricultural products for global supply chains, face the steepest surcharges at $135 per dry container. This creates cascading cost implications for companies relying on East African sourcing, from textiles and coffee to minerals and agricultural commodities. Shippers must now evaluate whether previously profitable sourcing strategies remain viable under new cost structures.

- East Africa: $135 dry / $200 refrigerated surcharges

- Red Sea: $60 dry / $90 refrigerated surcharges

- Indian sub-continent: $85 dry / $130 refrigerated surcharges

- Refrigerated container surcharges exceed dry container charges by 40-60 percent

War Risk Premiums and Rerouting: The Hidden Cost Multiplier

Beyond fuel surcharges, global shipping faces compounding cost pressures that logistics professionals must track separately. War risk premiums, now standard practice on vessels transiting high-risk regions, add insurance costs that sit outside traditional freight rate calculations. These premiums fluctuate based on geopolitical risk assessments and can add 1-3 percent to total logistics costs on affected routes.

The rerouting phenomenon itself creates indirect costs. When carriers extend voyage distances, they also extend transit times, increase crew fatigue costs, and require additional maintenance intervals on vessels. A 15-20 day voyage that extends to 25-30 days ties up vessel capacity and reduces annual container throughput per vessel. This reduced productivity must be offset through higher rates across the carrier’s entire fleet.

For supply chain planners, the critical insight is that fuel surcharges represent only one layer of cost escalation. When evaluating the true cost of ocean freight, professionals must integrate fuel surcharges, war risk premiums, potential detention charges due to extended transit times, and the opportunity cost of delayed inventory movement.

- War risk premiums add 1-3 percent additional costs

- Extended voyage distances increase per-container costs beyond fuel

- Vessel productivity declines with longer transits

- Total cost of freight exceeds published rate plus fuel surcharge

Strategic Implications for Supply Chain Leaders

The rise in ocean freight costs forces supply chain leaders to revisit fundamental strategic assumptions. For companies relying on cost-optimized Asian sourcing and European distribution, the economics of these networks are shifting. What was previously an optimal structure based on low Asian production costs plus economical ocean freight now faces margin compression from transportation costs.

There are several strategic responses available. First, companies can implement dynamic sourcing strategies that allow cargo to move via alternative routes based on real-time cost comparisons. Second, they can accelerate nearshoring initiatives to reduce dependence on intercontinental freight. Third, they can negotiate long-term freight agreements that lock in rates or create fuel surcharge caps.

Additionally, supply chain leaders should evaluate inventory positioning strategies. Higher freight costs make inventory holding at origin or destination more competitive compared to holding inventory in transit. Companies with flexible manufacturing or distribution capacity might benefit from shifting inventory forward into regional hubs during low-cost periods, reducing overall supply chain cost.

- Revisit cost assumptions underlying current sourcing strategies

- Evaluate dynamic routing options across multiple carriers

- Consider nearshoring as a long-term structural response

- Negotiate rate caps or fuel surcharge agreements with carriers

- Optimize inventory positioning based on new freight economics

Fuel Volatility as a Structural Market Feature

Perhaps the most important takeaway is recognizing that fuel volatility is not a temporary anomaly but increasingly a structural feature of global maritime markets. The integration of global energy markets, geopolitical fragmentation of trade lanes, and narrow carrier profit margins create conditions where fuel cost spikes transmit rapidly into freight rate increases.

Logistics professionals accustomed to the 2015-2020 period of sustained low bunker prices should recalibrate expectations. Fuel surcharge mechanisms, transparent pricing on bunker costs, and dynamic rate adjustments are becoming standard industry practices rather than exceptions. Companies that build organizational flexibility to absorb and respond to fuel volatility will maintain competitive advantage.

- Fuel volatility is structural, not cyclical, in current markets

- Fuel surcharges will remain standard carrier pricing mechanism

- Bunker fuel market transparency increasingly influences logistics strategies

- Supply chains require structural flexibility to manage recurring fuel shocks

Forward Outlook and Mitigation Strategies

Looking ahead, MSC’s decision to implement broad-based fuel surcharges signals that other carriers will likely follow with similar measures. This creates opportunities for shippers to negotiate, consolidate volume with specific carriers, or implement mode-shifting strategies before surcharges become more uniform across the industry.

Companies should establish fuel price monitoring protocols, create rate alert systems, and build relationships with carriers and freight forwarders who can provide advance warning of upcoming surcharges. Some carriers offer fuel surcharge caps for committed volume, which might provide cost certainty even if absolute rates remain volatile.

For immediate cost management, shippers can accelerate booking on routes not yet affected by surcharges, consolidate shipments to improve per-container economics, or shift lower-margin cargo to slower, more cost-efficient modes. The goal is maintaining supply chain fluidity while managing cost pressures actively rather than passively accepting rate increases.

- Monitor bunker fuel prices and carrier announcements closely

- Negotiate rate caps or fuel surcharge agreements immediately

- Consider forward bookings before surcharges expand

- Build redundancy across carriers to maximize negotiation leverage

- Establish dynamic routing protocols for mode and carrier selection