Indonesia’s Largest Petrochemical Producer Faces Critical Feedstock Constraint

Chandra Asri Pacific, Indonesia’s largest petrochemical producer, has declared force majeure, effectively announcing that it cannot meet contractual obligations due to extraordinary circumstances beyond its control. The force majeure declaration reflects a critical constraint in its primary feedstock supply-naphtha-which flows through the Strait of Hormuz from Middle East sources. With the Strait of Hormuz facing severe disruption, naphtha supply to Chandra Asri has been constrained, forcing the petrochemical producer to reduce production or suspend operations entirely. This declaration cascades through petrochemical supply chains dependent on Chandra Asri’s production.

Chandra Asri’s force majeure declaration is significant because it is explicit acknowledgment that a major petrochemical producer cannot operate normally due to energy supply constraints. The declaration provides legal protection for the company from contractual liability, but it simultaneously signals to customers, suppliers, and competitors that production is disrupted. The force majeure mechanism is designed for precisely this type of extraordinary circumstance-where external factors beyond an operator’s control prevent normal operations.

- Chandra Asri Pacific declares force majeure

- Strait of Hormuz disruption constraining naphtha feedstock supply

- Largest Indonesian petrochemical producer unable to operate normally

- Legal protection from contractual liability through force majeure

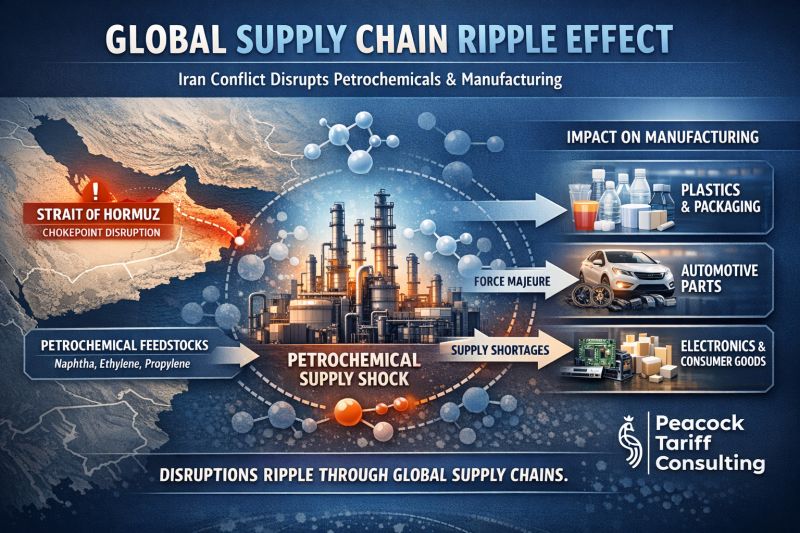

Naphtha Feedstock Dependency and Strait Vulnerability

Petrochemical production fundamentally depends on steady supplies of naphtha, a crude oil derivative that serves as the primary feedstock for ethylene production and ultimately plastics and synthetic materials. Naphtha is produced primarily in the Middle East, particularly from crude oil refineries in Saudi Arabia, Iraq, and other Gulf producers. Most naphtha exported globally passes through the Strait of Hormuz. Petrochemical producers in Asia, including Indonesia, depend on regular naphtha supplies sourced from Middle East producers and transported through the strait.

Chandra Asri’s vulnerability to Strait of Hormuz disruption reflects the geographic concentration of naphtha production. While Indonesia has crude oil reserves, naphtha yields are insufficient to support domestic petrochemical production at current levels. Chandra Asri therefore imports naphtha from Middle East suppliers, primarily via tanker transport through the Strait of Hormuz. This import dependency makes Chandra Asri vulnerable to any disruption in Hormuz shipping. Alternative naphtha sources exist, but they involve longer shipping distances, higher costs, or longer lead times.

- Naphtha produced primarily in Middle East

- Most global naphtha exports flow through Strait of Hormuz

- Indonesia relies on imported naphtha for petrochemical production

- Alternative naphtha sources more expensive or longer lead times

Cascading Supply Chain Disruption: Plastics, Automotive, Electronics, Consumer Goods

Chandra Asri produces ethylene and propylene, primary building blocks for plastics, synthetic fibers, and chemical intermediates. When Chandra Asri reduces production, the reduction cascades through plastic and polymer supply chains. Plastic film producers, resin manufacturers, fiber producers, and plastic product manufacturers that depend on Chandra Asri’s ethylene and propylene face feedstock constraints. These constraints force production reductions, inventory draws, or sourcing from alternative suppliers at higher costs. The supply chain disruption extends across plastic-dependent industries.

The plastic supply constraint affects automotive manufacturers requiring plastic components, electronics manufacturers requiring plastic housings and components, and consumer goods manufacturers requiring plastic packaging and materials. Automotive production slows due to component shortages. Electronics manufacturing faces delays due to plastic housing shortages. Consumer goods packaging becomes constrained. These cascading disruptions transform Chandra Asri’s force majeure declaration into a global supply chain constraint affecting multiple industries simultaneously. The scale of disruption extends far beyond petrochemical markets into end-user industries.

- Chandra Asri produces ethylene and propylene feedstocks

- Plastic producers depend on Chandra Asri output

- Automotive manufacturers depend on plastic components

- Electronics and consumer goods industries dependent on plastics

Petrochemical Price Inflation and Cost Pressures

Chandra Asri’s reduced production creates supply constraints that drive petrochemical price increases. With one of Asia’s largest petrochemical producers unable to operate at normal capacity, petrochemical supply becomes constrained relative to demand. Constrained supply drives price increases for ethylene, propylene, plastics, and polymer products. These price increases propagate through downstream supply chains, increasing costs for plastic-dependent manufacturers. The price inflation is immediate for spot market purchases and flows through contracted purchases over time.

The petrochemical price increases create cost inflation for manufacturing industries dependent on plastics and chemical inputs. Automotive manufacturers purchasing plastic components face higher input costs. Electronics manufacturers purchasing plastic housings face cost increases. Packaging manufacturers purchasing plastic films face elevated costs. Food and beverage manufacturers purchasing plastic packaging face increased input costs. The price inflation extends across multiple industries, creating economy-wide cost pressure from petrochemical supply constraints. These cost pressures are ultimately passed to consumers through higher product prices.

- Ethylene and propylene prices rising from constrained supply

- Plastic product prices increasing across categories

- Automotive component costs increasing

- Consumer-facing product prices rising from input inflation

Broader Force Majeure Risk and Supply Chain Reconfiguration

Chandra Asri’s force majeure declaration is likely to be followed by additional force majeure declarations from other petrochemical producers facing similar feedstock constraints. Petrochemical producers in Saudi Arabia, UAE, Qatar, and other Middle East locations may face their own feedstock and operational constraints as Strait of Hormuz disruptions persist. Additionally, producers in other regions dependent on Middle East naphtha supplies may face force majeure situations as naphtha supply becomes constrained. The cascade of force majeure declarations will expand petrochemical supply disruptions.

The force majeure cascade is driving petrochemical supply chain reconfiguration. Manufacturers dependent on petrochemical inputs are being forced to identify alternative suppliers, accept production constraints, or build inventory buffers. Some manufacturers are evaluating nearshoring petrochemical production to reduce import dependency. Others are exploring alternative materials that reduce plastic inputs. Still others are simply reducing production and accepting market share loss. These reconfiguration efforts are accelerated by the certainty that supply chain disruptions will persist as long as Strait of Hormuz disruptions continue.

- Additional force majeure declarations expected across sector

- Middle East producers facing similar feedstock constraints

- Asia-dependent producers evaluating alternative sourcing

- Nearshoring and alternative material strategies accelerating

Sourcing Alternatives and Long-Term Supply Chain Shift

In the near term, manufacturers facing Chandra Asri supply constraints are seeking alternative petrochemical suppliers. Options include producers in Saudi Arabia, Qatar, and other Middle East locations, but these producers are facing their own constraints. Asian petrochemical producers in Japan, South Korea, and China have capacity, but with current logistics constraints and elevated shipping costs, sourcing from these alternatives is expensive and slow. Some manufacturers are seeking spot market purchases at elevated prices from available suppliers. The combination of constrained supply, elevated costs, and logistics challenges creates an extremely difficult sourcing environment.

Long-term supply chain implications suggest significant reorganization. Companies are likely to pursue diversification of petrochemical supplier sources, nearshoring of plastic and chemical production, and inventory management strategies that provide buffers against supply disruptions. The current Strait of Hormuz disruption and resulting force majeure declarations are demonstrating the vulnerability of supply chains dependent on Middle East energy and petrochemical sources. This demonstration will likely drive permanent restructuring of supply chains to reduce this vulnerability. The changes will involve investment in new production capacity, nearshoring initiatives, and altered sourcing strategies.

- Alternative sourcing from Middle East, Asia options limited

- Spot market pricing extremely elevated

- Nearshoring initiatives accelerating

- Supplier diversification becoming strategic priority

Timeline and Resolution Scenarios

The duration of Chandra Asri’s force majeure depends on when Strait of Hormuz disruptions resolve. If strait disruptions resolve within weeks, naphtha supply normalizes and Chandra Asri can resume normal production, lifting the force majeure declaration. If disruptions persist for months, Chandra Asri faces extended production constraints, extended force majeure conditions, and significant customer impact. The resolution timeline is uncertain, but the risk of extended disruption is material.

Multiple scenarios are possible. Optimistic scenario: Strait disruptions resolve in April-May 2026, naphtha supply normalizes, Chandra Asri resumes normal production by mid-2026, and petrochemical markets normalize. Moderate scenario: Disruptions persist through summer 2026, extended supply constraints, significant supply chain impacts, and temporary force majeure. Pessimistic scenario: Disruptions persist indefinitely, multiple producers face extended force majeure, petrochemical markets restructure around constrained supply. The current trajectory suggests moderate to pessimistic scenarios more likely than optimistic resolution.

- Force majeure duration tied to Strait of Hormuz resolution

- Optimistic resolution: weeks to months, normalization by mid-2026

- Moderate scenario: extended disruption through summer

- Pessimistic scenario: indefinite supply constraints requiring restructuring