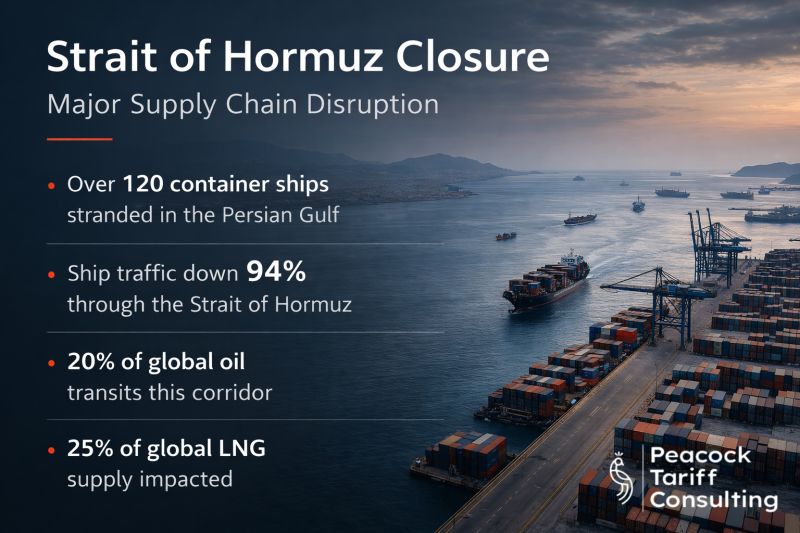

The Scale of the Strait of Hormuz Disruption

The Strait of Hormuz, the critical chokepoint through which approximately 21% of global oil and 20% of global liquefied natural gas (LNG) flows, faces extraordinary disruption that has paralyzed normal shipping operations. Over two million twenty-foot equivalent units of containerized cargo are currently trapped in the region, unable to move through the strait due to vessel movement restrictions and operational constraints. This represents a historic magnitude of cargo disruption affecting supply chains globally. More than 100 container vessels are waiting in queue to transit the strait, unable to proceed through normal channels.

Vessel movements through the Strait of Hormuz have declined approximately 90% from normal levels. Where 400-500 vessels typically transit the strait daily under normal conditions, current traffic has collapsed to roughly 40-50 daily movements. This dramatic reduction in vessel movements is a catastrophic disruption to one of the world’s most critical maritime chokepoints. The 90% reduction in vessel movements is a catastrophic disruption to one of the world’s most critical maritime chokepoints.

- Over 2 million TEU of cargo trapped in Strait region

- 100+ container vessels waiting to transit

- Vessel movements down 90% from normal levels

- 400-500 daily vessel transits reduced to 40-50

Critical Global Energy and Shipping Flows

The Strait of Hormuz represents a critical global chokepoint through which enormous quantities of energy and bulk commodities flow. Approximately 21 million barrels per day of crude oil pass through the strait, representing 21% of global seaborne oil trade. Liquefied natural gas exports from Qatar and other Middle East producers flow through the strait to global markets, with volumes approaching 90 million tonnes annually. Container vessels carrying manufactured goods from Asia to Europe and North America also transit the strait as part of major shipping routes. The concentration of global energy and trade flows through the strait makes disruptions catastrophic to global supply chains.

The strait’s criticality cannot be overstated. When the Strait of Hormuz is disrupted, no alternative transportation system can easily substitute for the 120 million tonnes of oil and refined products that normally transit monthly. Some oil can be redirected via overland pipelines from the Gulf to the Red Sea or Mediterranean, but pipeline capacity is limited. LNG cargoes can partially reroute via longer maritime routes around southern Africa, but this adds weeks to transit times and enormous additional costs. Container shipping cannot easily reroute because the strait represents the optimal path between Asian manufacturing centers and European and North American markets.

- Strait handles 21 million barrels per day of crude oil

- LNG exports from Qatar and Gulf producers dependent on strait

- Container vessels transiting for Asia-Europe, Asia-North America routes

- No adequate substitutes for strait capacity

Affected Ports and Regional Supply Chain Disruption

Major ports in the Persian Gulf region are directly affected by the Strait of Hormuz disruption. Jebel Ali in Dubai, one of the world’s largest container ports, faces backlog and congestion as vessels queue rather than transit. Dammam (Saudi Arabia), Hamad (Qatar), and Shuwaikh (Kuwait) are similarly affected. These ports normally experience steady flow of vessels transiting the region, but with strait transit severely restricted, vessels accumulate at ports unable to move cargo forward. Port congestion creates operational challenges for port operators and cargo backlogs for importers and exporters.

The port-level disruption creates secondary effects throughout regional supply chains. Importers waiting for cargo cannot clear shipments. Exporters cannot load goods for shipment. Regional manufacturers dependent on imported inputs face production halts due to input unavailability. Producers unable to export cannot clear inventory. These ripple effects throughout Middle East supply chains compound the direct effect of vessel movement restrictions. The regional supply chain disruption is immediate and severe.

- Jebel Ali, Dammam, Hamad, Shuwaikh ports experiencing severe backlog

- Port congestion from vessels unable to transit

- Regional importers unable to clear shipments

- Exporters unable to move goods creating production pressure

Container Delays and Schedule Disruption

Containerized cargo delays extend far beyond the immediate strait region. Container vessels that normally transit the Strait of Hormuz as part of regular service cycles are delayed by weeks or forced to reroute around southern Africa or through overland networks. These routing alternatives add 15-25 days to typical transit times. Shippers expecting cargo within three weeks face delays approaching five or six weeks. These schedule disruptions create cascading delays throughout supply chains as cargo dependent on timely arrival is delayed.

The delays create operational challenges for importers, manufacturers, and retailers. Companies with just-in-time supply chain models face production halts due to delayed input arrivals. Retailers dependent on timely inventory replenishment experience stockouts. Manufacturers unable to receive inputs cannot fulfill customer orders. These cascading operational disruptions extend the Strait of Hormuz constraint far beyond shipping logistics into production and retail operations. The magnitude of delay creates supply chain breaks that affect end consumers.

- Container transit times increasing 15-25 days

- Three-week transits becoming five-six week transits

- Cascading supply chain delays affecting manufacturers and retailers

- Just-in-time supply chains experiencing production halts

Insurance Premiums and Risk Pricing

Vessel owners and operators attempting to transit the Strait of Hormuz face increased insurance premiums reflecting elevated risk. War risk insurance, hull insurance, and cargo insurance all reflect higher premiums when vessels are exposed to the Strait of Hormuz disruption. These insurance cost premiums are passed through to shippers and ultimately to importers and consumers. The increase in insurance costs adds 1-3% to total shipping costs for routes transiting the strait. Over the volume of cargo normally flowing through the strait, these insurance cost increases aggregate to billions of dollars annually.

The elevated insurance costs create an additional disincentive for vessel operators to transit the strait. The combination of reduced vessel speeds, increased queueing delays, and elevated insurance costs makes the strait route substantially more expensive. Some shipowners and operators are choosing to reroute cargo around southern Africa despite the 15-25 day additional transit time, because the alternative routes have lower insurance costs and risk profiles. The insurance cost premium is therefore functioning as an additional constraint limiting strait traffic beyond pure physical restrictions.

- War risk insurance premiums elevated significantly

- Hull and cargo insurance costs increased 1-3%

- Insurance costs aggregating to billions across affected cargo

- High insurance costs incentivizing alternative routing

Secondary-Order Effects: Equipment Shortages and Rate Volatility

The Strait of Hormuz disruption creates secondary effects throughout global shipping and logistics. Container equipment shortages develop as containers accumulate in the region unable to move forward. If containers are stuck in queue waiting for strait transit, they are unavailable in other regions, creating container shortages elsewhere. These shortages increase the cost of shipping from unaffected regions. The container shortage also constrains shipping capacity by reducing the pool of available equipment.

Shipping rate volatility increases as operators manage constrained capacity and uncertain routing. Spot market shipping rates fluctuate dramatically based on available capacity, routing alternatives, and cargo demand. The uncertainty of strait transit creates premium rates for goods requiring guaranteed delivery. The combined effect of equipment shortages, elevated insurance costs, and rate volatility creates an extremely expensive and uncertain shipping environment. Shippers facing unknown costs and uncertain timelines are retreating from cost-optimized shipping practices toward more expensive but reliable alternatives.

- Container equipment shortages developing globally

- Shipping rate volatility increasing across markets

- Premium rates for guaranteed delivery creating cost pressure

- Shippers shifting to expensive reliable alternatives

Global Supply Chain Ripple Effects and Strategic Implications

The Strait of Hormuz disruption extends far beyond the immediate region. Energy prices globally are affected by constrained oil and LNG exports from the Gulf. Manufacturing costs globally are affected by delayed component arrivals. Retail supply globally is affected by container delays. The disruption creates global supply chain uncertainty and cost inflation. Companies worldwide are reassessing supply chain strategies in light of demonstrated vulnerability of critical chokepoints.

The disruption is driving strategic reconsideration of supply chain resilience. Companies are evaluating whether excessive concentration in Asian manufacturing is prudent given the vulnerability of maritime chokepoints. Others are evaluating nearshoring strategies that reduce reliance on long-distance shipping. Still others are evaluating inventory buffer strategies that provide resilience against transit disruptions. The Strait of Hormuz disruption is creating lasting effects on supply chain strategy, not merely temporary logistical challenges.

- Global energy prices affected by constrained exports

- Manufacturing delays affecting industries worldwide

- Retail supply disruptions creating consumer-level impacts

- Strategic supply chain reconfiguration underway