Transpacific Capacity Withdrawal Signals Demand Shock

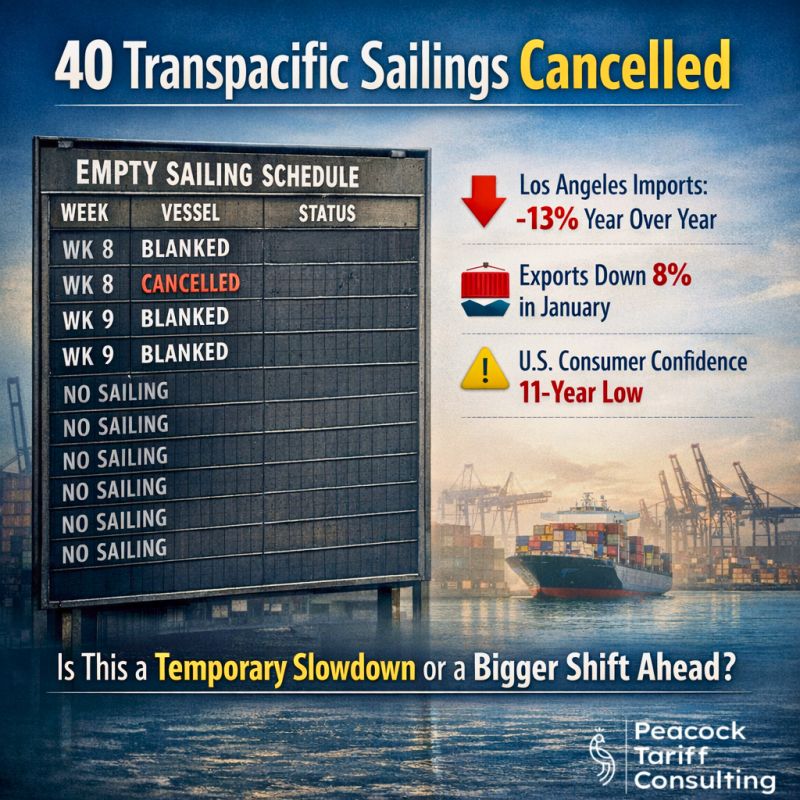

Container shipping lines operating transpacific routes have cancelled nearly 40 sailings, representing a significant withdrawal of capacity from Asia-North America trade lanes. This capacity reduction reflects softening import demand from the United States and weakening overall transpacific trade volumes. The cancellation of scheduled sailings indicates that shipping lines have concluded that demand no longer justifies deploying full vessel capacity on these traditionally high-volume routes. This decision to deliberately reduce service frequency represents a substantial shift in transpacific shipping dynamics.

The decision to cancel nearly 40 sailings is not merely an operational adjustment but a strategic statement about future demand expectations. Container lines order vessels years in advance based on expected trade volumes. When lines withdraw capacity, they are signaling reduced expectations for near-term demand. The scale of the capacity reduction-nearly 40 sailings-translates to removal of approximately 200,000-250,000 TEU (twenty-foot equivalent units) of monthly capacity from transpacific routes. This reduction is significant relative to total transpacific capacity.

- Nearly 40 transpacific sailings cancelled by container lines

- Capacity removal totaling 200,000-250,000 monthly TEU

- Reflects explicit demand weakness expectations

- Most significant capacity reduction in recent years

Port of Los Angeles Import Contraction

The Port of Los Angeles, America’s largest container port, experienced import volume declines of 13% year-over-year in January 2026, providing concrete evidence of weakening transpacific demand. Los Angeles imports declined from 900,000 TEU in January 2025 to approximately 785,000 TEU in January 2026. This magnitude of decline represents a substantial reduction in merchandise imports flowing through the primary US West Coast port. The consistent decline across a diversified mix of import categories indicates systemic demand weakness rather than product-specific disruption.

Export volumes from Los Angeles declined 8% year-over-year, representing a smaller decline than imports but still meaningful evidence of trade weakness. Exports from Los Angeles totaled approximately 540,000 TEU in January 2026, down from 587,000 TEU in January 2025. The simultaneous decline in both imports and exports indicates that transpacific trade weakness is comprehensive rather than limited to inbound shipments. The symmetry of weakness across both directions suggests that underlying macroeconomic factors are depressing total trade volumes.

- LA port imports down 13% year-over-year

- LA port exports down 8% year-over-year

- January 2026 weakest month in 3 years

- Both import and export weakness indicating systemic demand decline

Consumer Confidence Collapse and Demand Destruction

The underlying driver of transpacific shipping capacity reduction and port volume declines is consumer confidence collapse. Consumer confidence indices have reached lowest levels in over a decade, indicating pervasive pessimism about economic conditions and future purchasing power. When consumer confidence collapses, retail purchasing declines, leading to reduced demand for imported consumer goods. Retailers place fewer orders for imported products, cancel planned purchases, and reduce inventory positions. This reduced retail demand immediately translates into reduced container shipping volumes from Asia to North America.

The consumer confidence metric is particularly relevant for transpacific shipping because consumer goods represent a substantial share of transpacific imports. Apparel, footwear, furniture, toys, electronics, and countless other consumer products move from Asian manufacturing centers to US retailers via transpacific container ships. When consumer confidence collapses to multi-decade lows, retailers reduce orders for these products. The ordering reduction creates immediate reductions in transpacific container volumes as fewer containers move from Asia to the US.

- Consumer confidence at lowest levels in over a decade

- Retail purchasing declining from confidence weakness

- Retailers cancelling orders and reducing inventory

- Consumer goods imports concentrated in transpacific trade

Capacity Adjustment and Sailing Frequency Reduction

Container lines have responded to weakening transpacific demand by reducing weekly sailing frequency on major transpacific routes. Instead of deploying sufficient capacity for multiple sailings per week from major Asian ports to US West Coast ports, lines have consolidated shipments, stretched sailing schedules, and cancelled services where demand no longer justifies operation. Some lines have moved vessels to other trade lanes perceived as having stronger demand. This redeployment of vessels away from transpacific routes represents a fundamental shift in how container lines allocate capital and assets.

The reduction in sailing frequency creates operational challenges for shippers and manufacturers. Fewer weekly sailings mean that shippers must wait longer for available container space or consolidate shipments across longer time periods. This operational friction increases costs and reduces supply chain flexibility. However, the lines have concluded that maintaining high sailing frequency with reduced demand utilization is uneconomical. The trade-off between high frequency and full utilization has shifted in favor of reduced frequency and fuller vessel utilization.

- Weekly sailing frequency reduced on major transpacific routes

- Vessels redeployed to higher-demand trade lanes

- Fewer sailings increasing shipper wait times

- Lines optimizing for vessel utilization over frequency

Capacity Expected to Return in March: A Fragile Recovery Signal

Container lines have signaled that transpacific capacity is expected to return in March 2026, suggesting optimism that demand weakness may be temporary. This capacity restoration would indicate that lines expect demand to strengthen in March or anticipate inventory replenishment needs in the spring season. However, the fragility of the capacity return signal should not be underestimated. If demand does not recover as expected, lines will quickly reduce capacity again. The temporary nature of the capacity reduction and the conditional nature of the March recovery signal indicate that demand weakness is seen as cyclical rather than structural.

The March capacity recovery signal should be understood as conditional and subject to revision based on incoming demand data. If container availability remains weak, booking rates remain low, and consumer demand signals remain negative, lines may further reduce frequency or maintain reduced capacity. The March signal reflects hope for recovery rather than confidence in recovery. This conditional optimism indicates that shipping lines see current demand weakness as potentially temporary but are prepared to adjust rapidly if recovery does not materialize.

- Capacity expected to return in March if demand recovers

- Recovery signal conditional on demand improvement

- Further capacity cuts possible if demand remains weak

- Lines prepared for rapid adjustment to demand changes

Broader Supply Chain Implications

The transpacific shipping capacity reduction and port volume declines signal significant challenges for supply chains dependent on Asian imports. Retailers and manufacturers that depend on timely Asian shipments face operational difficulties when sailing frequency declines. Inventory positions become harder to manage, supply chain buffers shrink, and contingency planning becomes more complex. These operational challenges translate into higher costs for companies managing supply chains and uncertainty for businesses managing inventory cycles.

The capacity reduction also has implications for Asia-based manufacturers and exporters. Reduced shipping capacity means reduced ability to export merchandise to the US market. This capacity constraint may preserve margins for shipping lines, but it creates challenges for exporters unable to move products despite having demand. The reduced capacity functions as a bottleneck constraining export-oriented production in Asia. If capacity reductions persist, Asian manufacturers may need to adjust production levels or seek alternative shipping routes.

- Retailer inventory management more challenging

- Supply chain wait times increasing materially

- Asian exporters facing shipping bottlenecks

- Alternative shipping routes becoming more attractive